The process of securing a loan can be complex, and a well-drafted Consumer Loan Agreement Template is absolutely crucial for protecting both the borrower and the lender. This template provides a solid foundation for establishing clear terms and conditions, minimizing potential disputes, and ensuring a legally sound transaction. Consumer Loan Agreement Template is more than just a document; it’s a roadmap for a successful loan relationship. Understanding the nuances of this agreement is paramount for anyone considering borrowing money. This guide will delve into the key components, best practices, and potential pitfalls associated with creating and reviewing a Consumer Loan Agreement Template. We’ll explore how to tailor the template to specific loan types and scenarios, emphasizing the importance of legal counsel when necessary. Remember, this is a starting point – always consult with a legal professional to ensure your agreement complies with all applicable laws and regulations.

A comprehensive Consumer Loan Agreement Template typically includes several key sections. Each section addresses a critical aspect of the loan transaction. Let’s break down the essential elements:

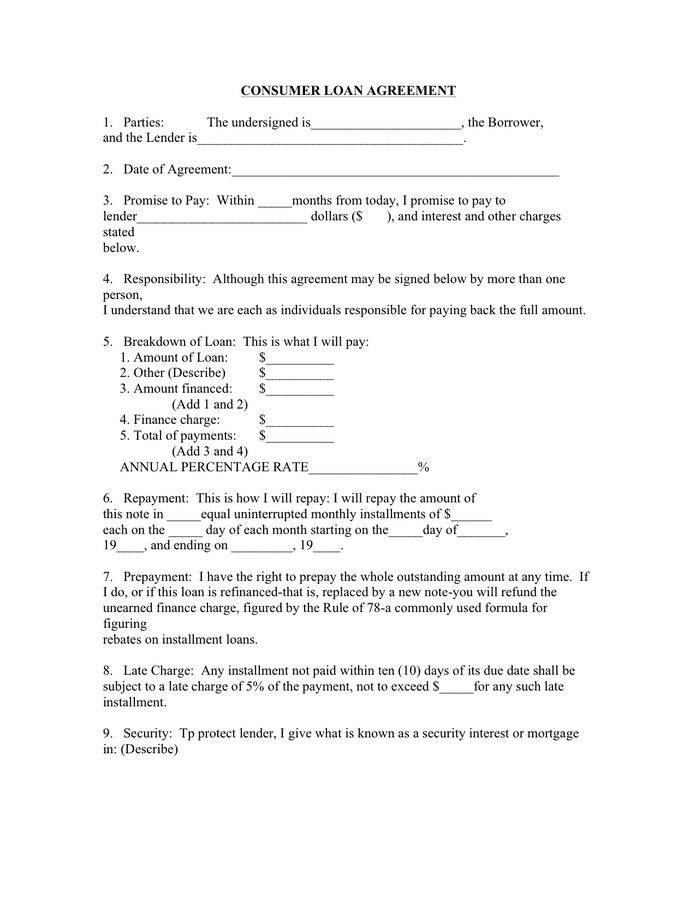

The initial section of the agreement should clearly state the loan amount, the type of loan (e.g., personal loan, auto loan, mortgage), and the purpose for which the funds are being borrowed. It’s crucial to avoid ambiguity. For example, instead of simply stating “a loan,” specify “a personal loan for $10,000 to purchase a new vehicle.” The lender should also provide a detailed breakdown of all fees associated with the loan, including origination fees, application fees, and any other charges. This transparency is vital for both parties. A template should include a space for the borrower to specify the intended use of the funds.

The repayment schedule is a cornerstone of the agreement. The agreement should clearly state the frequency of payments (e.g., monthly, bi-weekly), the payment amount, and the due date for each payment. A variable interest rate agreement should be clearly defined, outlining how the interest rate will change over time. Consider including a clause that allows for adjustments to the repayment schedule due to unforeseen circumstances. A good example is a clause that allows for a grace period of 30 days after the due date before late fees are assessed.

This section is critical for outlining the lender’s rights if a borrower fails to meet their obligations. It should clearly define what constitutes a default, including missed payments, late payments, and other breaches of the agreement. The agreement should specify the lender’s remedies, which may include:

If the loan is secured by collateral, such as a vehicle or property, the agreement should clearly outline the collateral, its value, and the lender’s rights to seize and sell the collateral if the borrower defaults. The lender should provide a detailed appraisal of the collateral to ensure its value is accurately represented. A well-documented appraisal is essential for protecting the lender’s investment. The agreement should also specify the process for transferring ownership of the collateral to the lender in the event of a default.

This section specifies which state’s laws will govern the agreement and outlines the process for resolving disputes. It’s often advisable to include a clause that requires mediation before resorting to arbitration or litigation. Mediation offers a more amicable and cost-effective way to resolve disputes. The agreement should also specify the jurisdiction where any disputes will be resolved. Consider including a clause that allows for arbitration, which is generally faster and less expensive than litigation.

This section protects both parties by outlining the confidentiality of information shared during the loan process. It should specify that all communications and documents related to the loan will be treated as confidential and not disclosed to third parties without the borrower’s consent.

Creating a robust Consumer Loan Agreement Template is a vital step in securing a successful loan relationship. By carefully considering each section and tailoring the agreement to the specific loan and borrower, you can minimize risks and protect both parties. Remember that this template is a starting point – always seek legal counsel to ensure compliance with all applicable laws and regulations. A well-drafted agreement not only protects your interests but also fosters trust and transparency within the lending process. Proper documentation and clear communication are key to a smooth and successful loan transaction. Ultimately, a thoughtfully constructed agreement demonstrates professionalism and a commitment to responsible lending practices. Investing in legal review is a smart move to safeguard your financial well-being.