Borrowing money can be a significant financial undertaking, and establishing a clear, legally sound contract is paramount to protect both the borrower and the lender. A well-drafted legal contract template for borrowing money provides a framework for understanding obligations, responsibilities, and potential risks. This article will guide you through the essential components of a robust contract, emphasizing the importance of legal counsel and best practices. Legal Contract Template For Borrowing Money is a critical tool for anyone seeking to secure a loan or financing arrangement. It’s not simply a formality; it’s a vital safeguard against disputes and misunderstandings. Understanding the nuances of contract law is crucial for ensuring a fair and equitable outcome. Furthermore, choosing the right template and ensuring it’s tailored to your specific circumstances significantly increases the likelihood of a successful loan agreement. This guide will cover key elements, offering practical advice and highlighting the role of experienced legal professionals.

The process of creating a legal contract for borrowing money involves several key steps. First, clearly define the amount of the loan, the purpose of the borrowing, and the repayment terms. Next, establish the borrower’s obligations, including maintaining insurance, providing collateral, and adhering to any specific rules or regulations. Finally, outline the lender’s rights and responsibilities, including the right to access the funds and the consequences of default. It’s vital to remember that this is a starting point; the specific terms should be negotiated and tailored to the individual circumstances of the transaction. Consulting with a qualified attorney is highly recommended, especially for larger loans or complex situations.

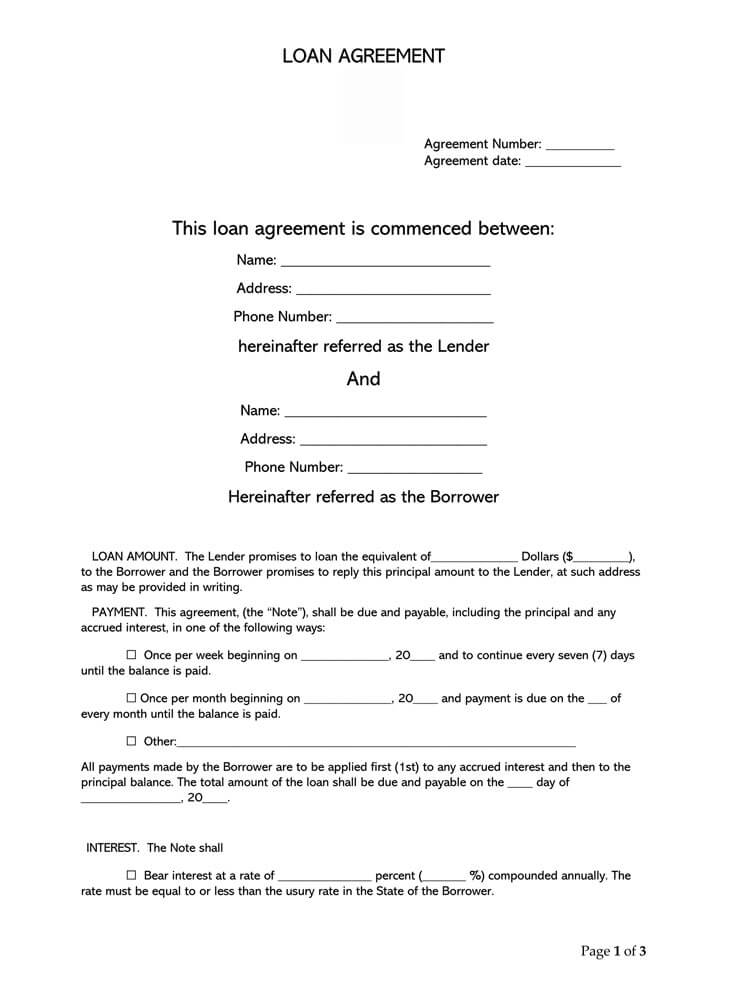

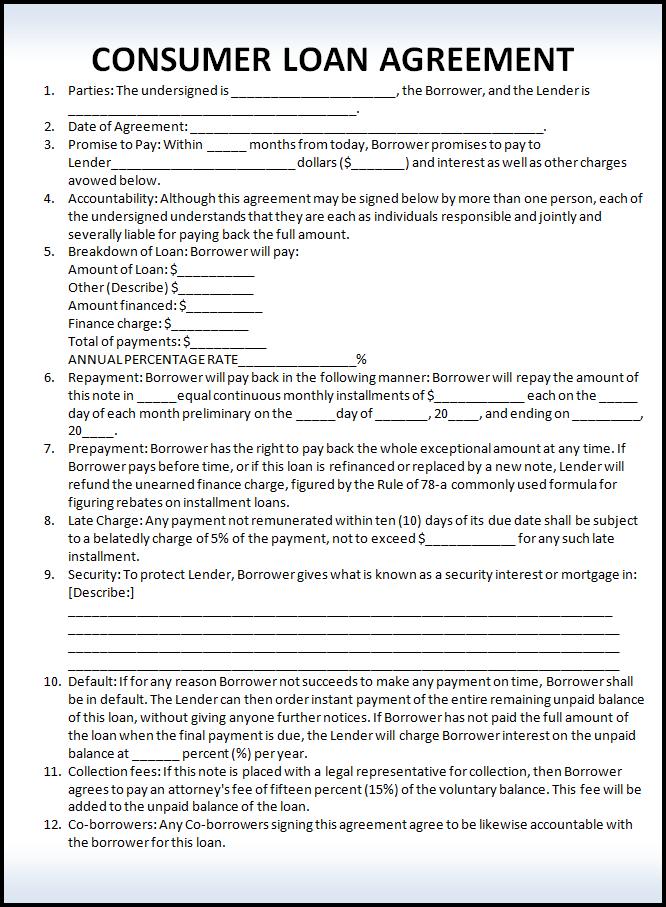

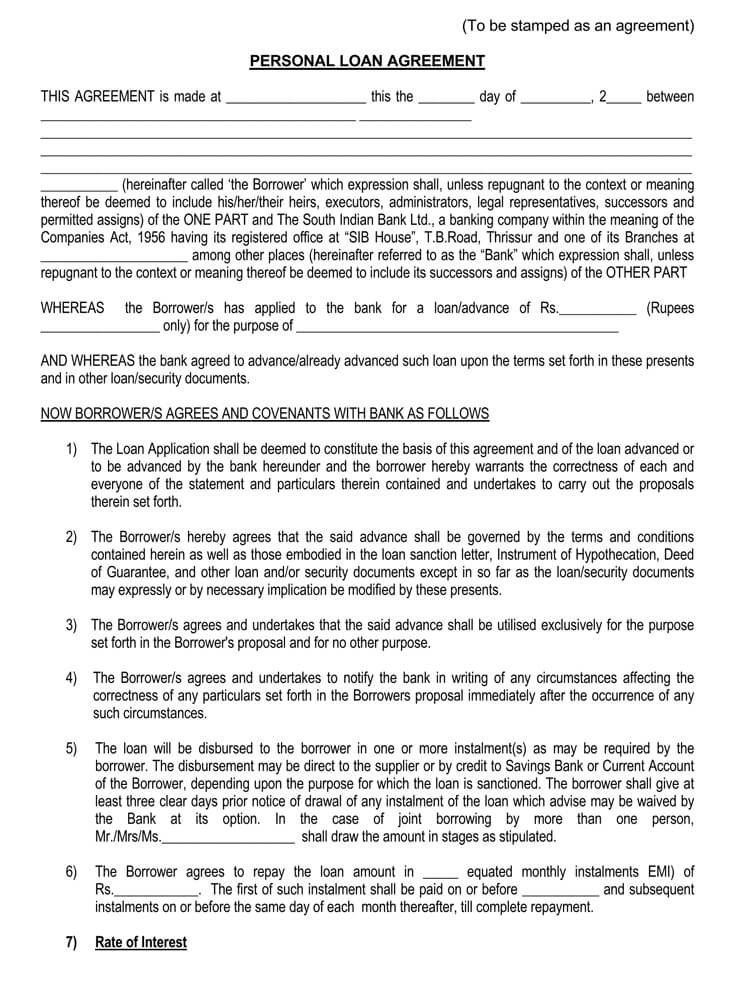

A comprehensive legal contract for borrowing money typically includes several core components. These elements ensure clarity, accountability, and protect both parties involved. The first and most fundamental element is the loan agreement, which formally outlines the terms of the loan. This agreement should clearly state the principal amount, the interest rate (if any), the repayment schedule, and the consequences of late or missed payments. The language used should be precise and unambiguous to avoid any room for misinterpretation. A well-drafted loan agreement should also address any potential penalties for breach of contract.

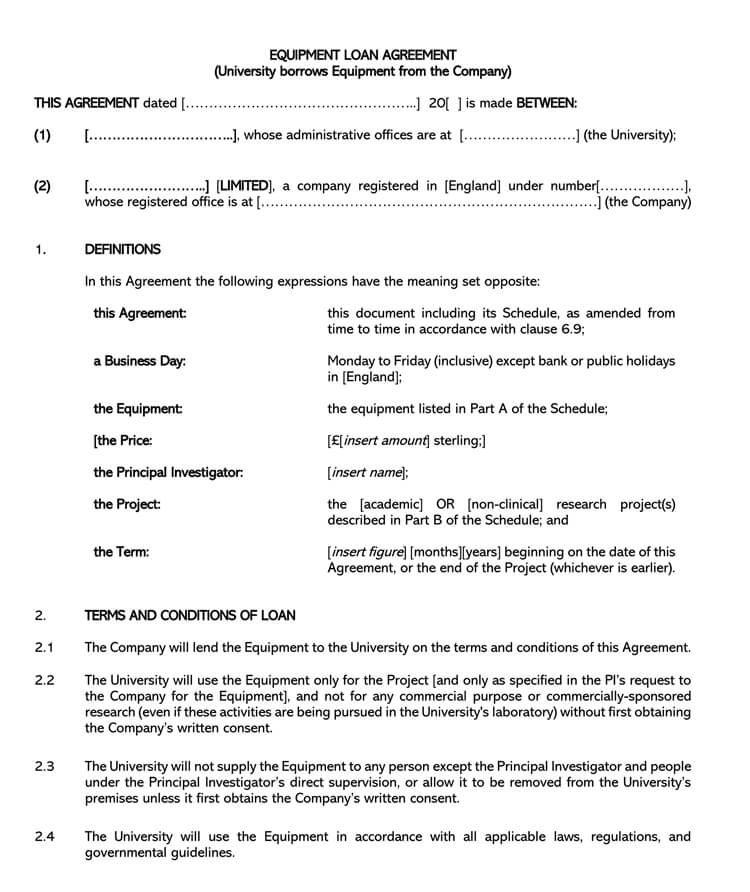

Beyond the basic agreement, several other crucial elements are included. Collateral is a frequently discussed aspect, and the contract must clearly define what constitutes collateral and its value. If collateral is involved, the contract should specify the process for valuing and securing the collateral. Default provisions outline the consequences if one party fails to fulfill their obligations. These provisions can include late payment fees, repossession rights, or other remedies. Governing law specifies which jurisdiction’s laws will govern the interpretation and enforcement of the contract. Choosing the appropriate governing law is important, as it can significantly impact the legal consequences of a breach.

The language used in a legal contract is just as important as the contract itself. Ambiguous or overly complex language can lead to disputes and legal challenges. It’s crucial to use plain language that is easily understood by all parties involved. Avoid jargon and technical terms that may not be familiar to everyone. When possible, use bullet points or numbered lists to break down complex information. Furthermore, be specific and avoid vague statements. Instead of saying “We will make payments,” state “Payments will be made on the first day of each month, commencing on January 1, 2024.”

Consider the potential for misunderstandings. A contract that is too convoluted or difficult to understand can lead to disagreements and delays. It’s always best to seek legal advice to ensure that the contract is clear and unambiguous. A lawyer can review the contract and identify any potential issues that may arise. They can also help to negotiate terms that are fair and equitable to both parties. A poorly written contract can be a significant source of conflict and expense.

Interest rates are a significant factor when considering a loan for borrowing money. The interest rate represents the cost of borrowing and can significantly impact the overall cost of the loan. A higher interest rate means a higher cost for the borrower. It’s important to understand the type of interest rate being charged – fixed or variable. Fixed-rate loans offer a consistent interest rate throughout the loan term, while variable-rate loans can fluctuate based on market conditions. Be sure to clearly outline the interest rate structure and any associated fees.

Beyond the interest rate, other fees can also be included in the contract. These fees can include origination fees, application fees, appraisal fees, and closing costs. It’s important to understand all of the fees associated with the loan and to negotiate them to ensure they are reasonable. A detailed breakdown of all fees should be included in the contract. Failure to disclose fees can be a breach of contract.

A default clause is a critical section of a loan agreement that outlines the consequences if a borrower fails to meet their obligations. These clauses can range from a simple notification of default to a more formal legal action. It’s essential to understand the specific terms of the default clause and to ensure that it aligns with your expectations. The clause should clearly state the remedies available to the lender, such as repossession or acceleration of the loan. It should also specify the timeframe within which the borrower must rectify the default.

Furthermore, consider the penalty clause, which outlines the financial penalties for late payments or other breaches of contract. These penalties can be substantial and can significantly impact the borrower’s financial situation. A well-defined penalty clause can help to protect the lender’s interests. However, it’s important to ensure that the penalty is reasonable and proportionate to the breach of contract.

Given the complexity of legal contracts, it’s crucial to seek legal review before signing any agreement for borrowing money. A lawyer can review the contract to ensure that it is legally sound and protects your interests. They can also advise you on the terms of the contract and negotiate them to ensure they are fair and equitable. Many lenders require borrowers to have their contracts reviewed by an attorney before signing. This is a standard practice and can help to prevent disputes and legal challenges.

Don’t hesitate to ask questions. If you don’t understand something in the contract, seek clarification from your attorney or the lender. It’s always better to be proactive and ensure that you have a clear understanding of your rights and obligations. A poorly drafted contract can lead to significant problems down the road.

In today’s digital age, utilizing technology to manage contracts can significantly improve efficiency and reduce the risk of errors. Contract management software can automate many of the tasks involved in contract creation, review, and execution. These tools often include features such as automated workflows, document storage, and audit trails. By implementing a contract management system, you can ensure that all contracts are properly documented and that all parties are aware of their obligations. This can also help to streamline the loan approval process and reduce the time it takes to close a deal.

The legal landscape surrounding borrowing money is subject to various regulations and compliance requirements. Consumer protection laws and financial regulations can impact the terms of a loan agreement. It’s important to be aware of these regulations and to ensure that your contract complies with all applicable laws. For example, certain types of loans may be subject to disclosure requirements or restrictions on interest rates. Staying informed about regulatory changes is essential for protecting your business and ensuring compliance.

Establishing a robust legal contract for borrowing money is a critical step in securing a successful loan. By carefully considering the core components, prioritizing clear and concise language, understanding the implications of interest rates and fees, and seeking professional legal advice, you can significantly increase the likelihood of a favorable outcome. Remember that a well-drafted contract is an investment in your financial future. Ultimately, a legally sound agreement provides a foundation for a stable and trustworthy relationship with your lender. Don’t underestimate the importance of protecting your interests – a strong contract is a powerful tool for achieving your financial goals.