Navigating complex financial transactions, whether in real estate, business acquisitions, or international trade, often requires a formal demonstration of liquid assets. For these critical moments, having a clear, verifiable Proof Of Funds Letter Template readily available can significantly streamline processes and build immediate credibility with counterparties. This essential document serves as an official declaration, issued by a financial institution, confirming that an individual or entity possesses the necessary capital to complete a specified transaction. Understanding how to secure, structure, and utilize this letter is paramount for efficient deal-making in today’s fast-paced financial landscape.

The necessity for a Proof of Funds (POF) letter stems from the need for assurance. Sellers, landlords, and investors want confirmation that a potential buyer isn’t wasting their time or resources with an offer that lacks backing. A well-prepared POF letter bridges this gap, moving a proposal from a mere intention to a serious, qualified undertaking. Its structure must be professional, concise, and undeniably authentic, often requiring the letterhead and signature of a recognized banking institution.

This comprehensive guide will explore the intricacies surrounding the POF letter, detailing its components, the types of financial institutions that issue them, and practical advice on how to deploy this tool effectively. We will examine the critical elements that elevate a simple statement into an authoritative financial document that can unlock significant opportunities.

A Proof of Funds letter is far more than a simple bank statement; it is a formal attestation from a bank or recognized financial entity regarding the availability of specific liquid assets under the account holder’s control. Its primary function is to eliminate ambiguity regarding a buyer’s financial capacity for a transaction.

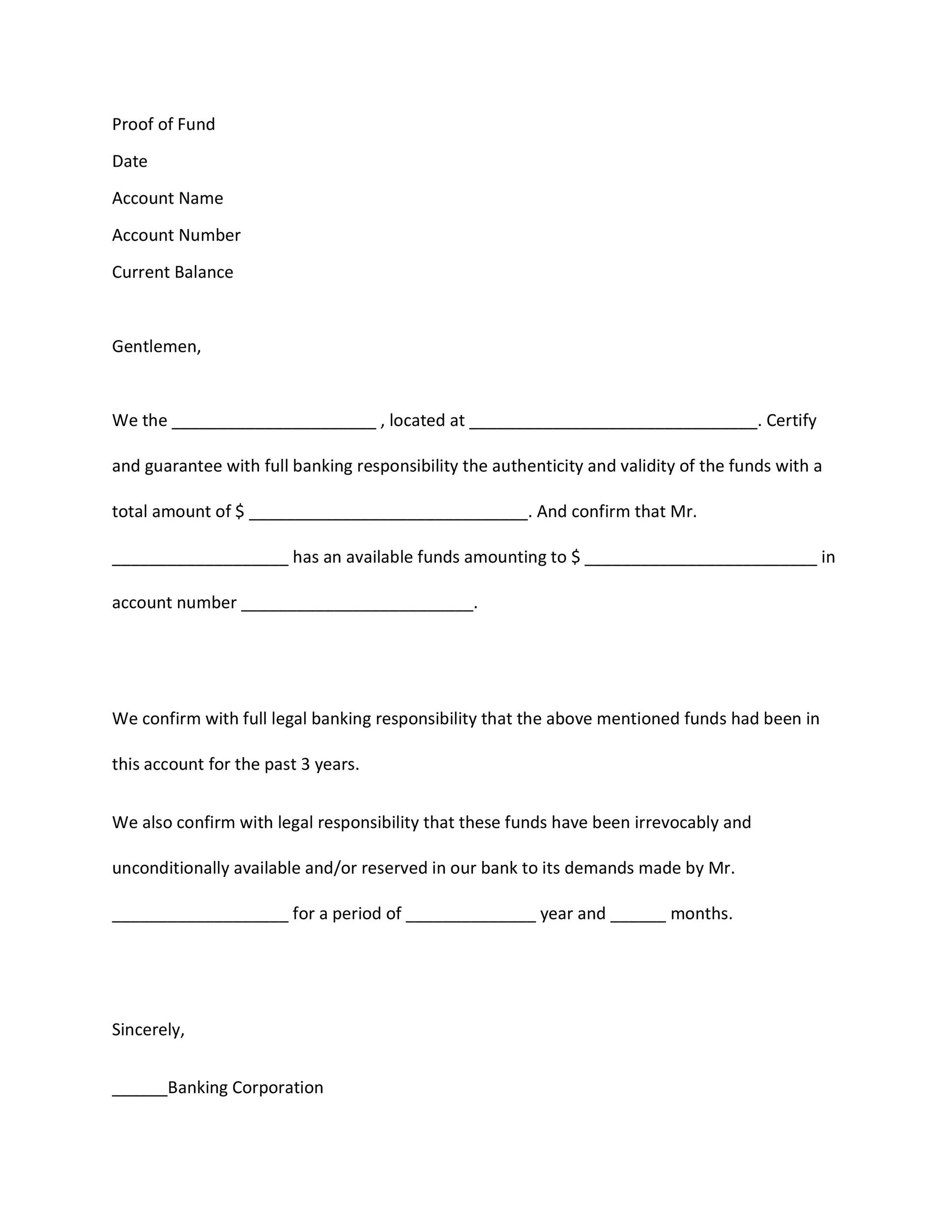

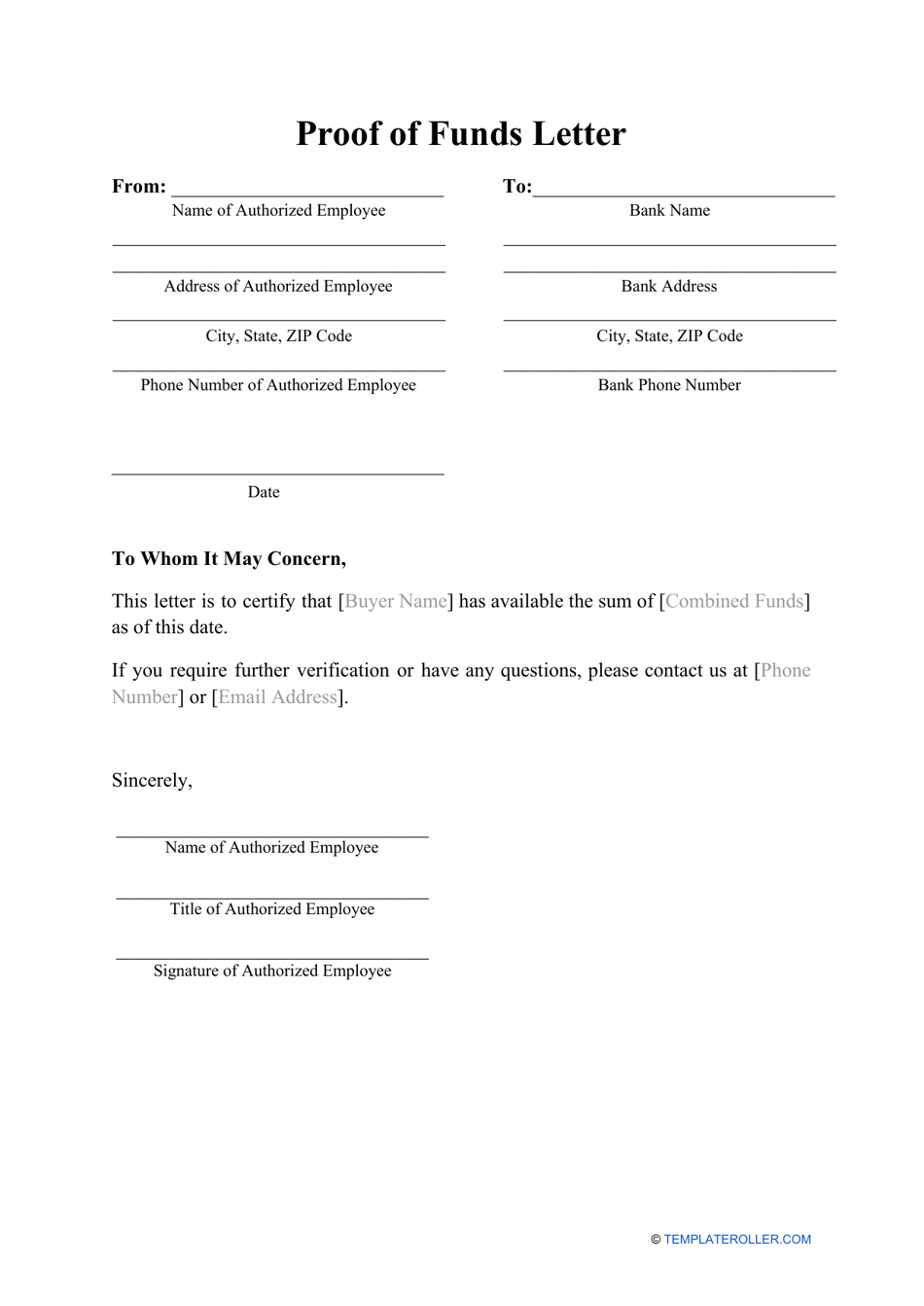

While the specifics might vary depending on the issuing bank and the nature of the transaction, several core elements are universally required for a valid Proof of Funds letter. Missing any of these can lead to immediate rejection by sophisticated sellers or escrow agents.

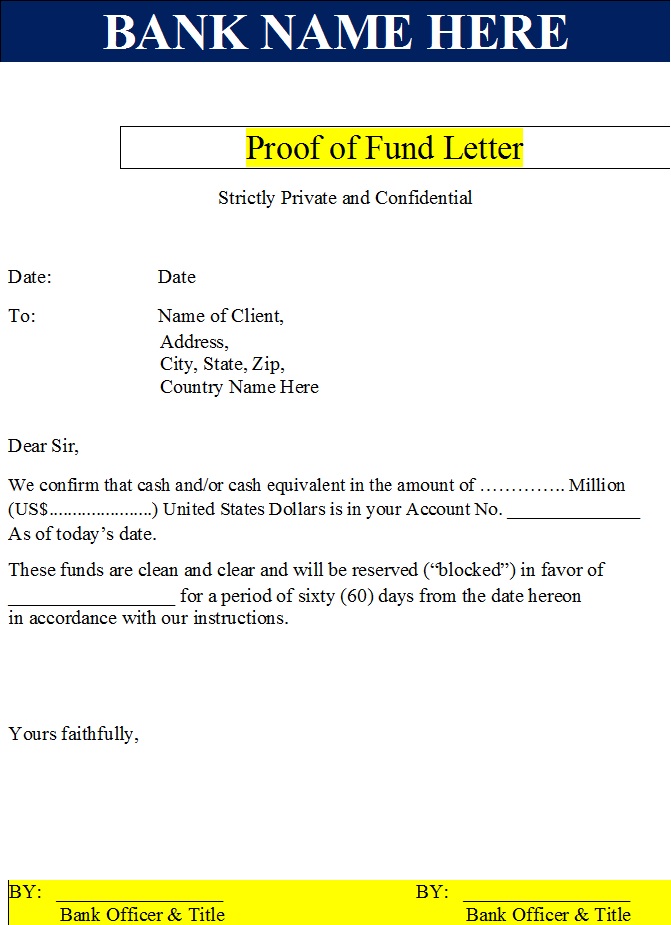

First, the letter must prominently feature the official letterhead of the issuing financial institution, including contact details, routing numbers, and SWIFT codes if applicable. Second, it must clearly state the date of issuance, as these documents often have short validity periods, sometimes only 10 to 30 days.

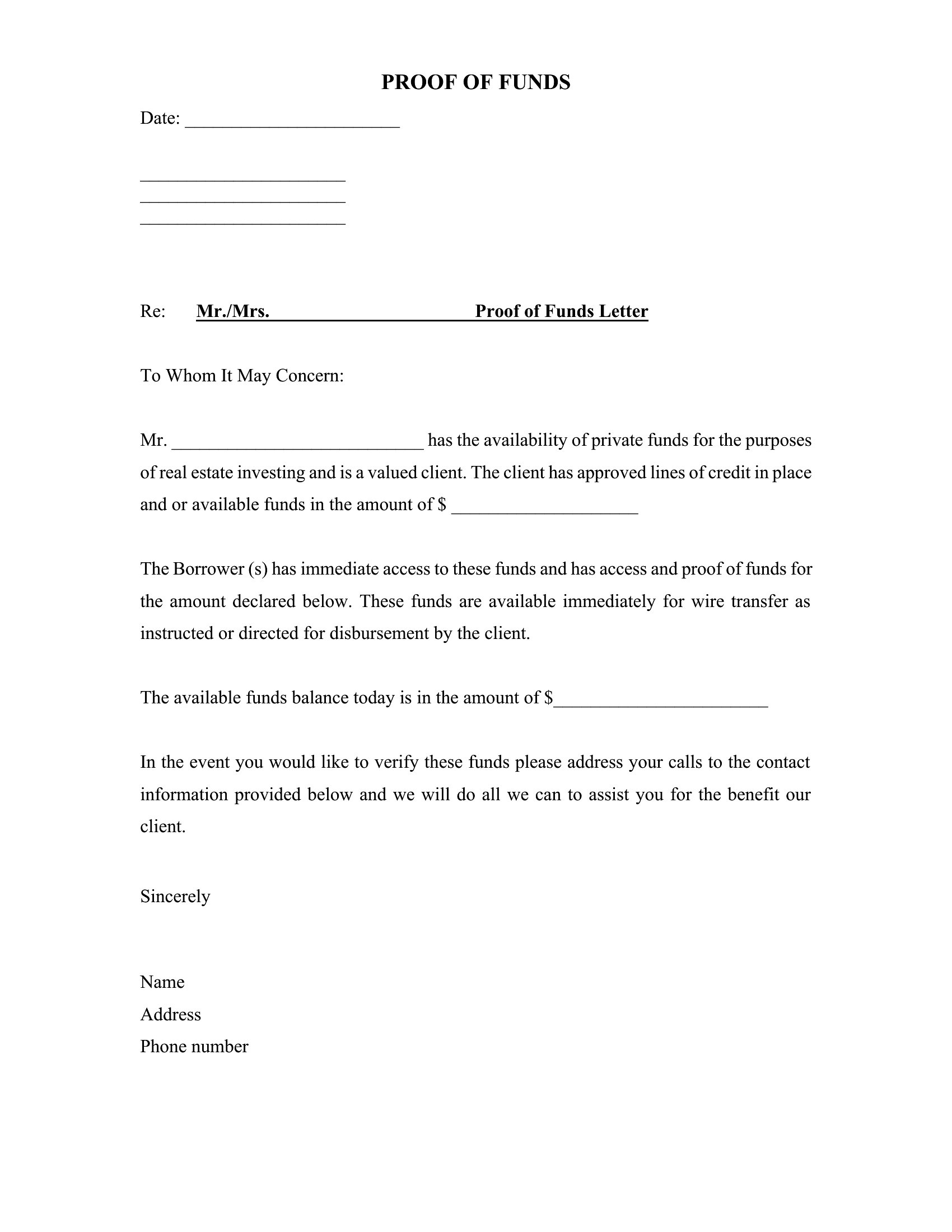

Crucially, the letter must identify the account holder (the individual or company seeking to prove funds) accurately. It must then explicitly state the total verifiable amount of liquid assets available. This figure is often stated in both numerical and written form to prevent alteration. Finally, the letter must contain an authorized signature and title from a bank officer authorized to make such certifications, lending the necessary institutional weight to the document.

It is essential to distinguish a POF letter from a standard bank account statement. A bank statement shows a history of transactions—deposits, withdrawals, and balances over time. While useful for due diligence, it doesn’t definitively confirm that the funds are currently liquid and unencumbered for a specific purchase on the day of presentation.

In contrast, the Proof of Funds letter is a snapshot in time, explicitly certifying that the stated amount is presently available and accessible to the account holder for the intended purpose. This focused assurance is what makes the POF letter the preferred instrument for high-value negotiations.

The demand for a POF letter is highest in sectors where large sums of capital are moved quickly and where confirmation of liquidity is a prerequisite for serious engagement. Real estate investment leads this charge, but it extends far beyond residential property sales.

In commercial real estate, sellers of large office buildings, industrial parks, or multi-family housing developments demand POF to ensure that bidders have the capacity for down payments, earnest money, or outright purchase. Similarly, when a company seeks to acquire another business—whether through a stock purchase or asset acquisition—the target company’s shareholders or board will require POF from the acquiring entity to confirm the financing is secure before granting extensive access for due diligence.

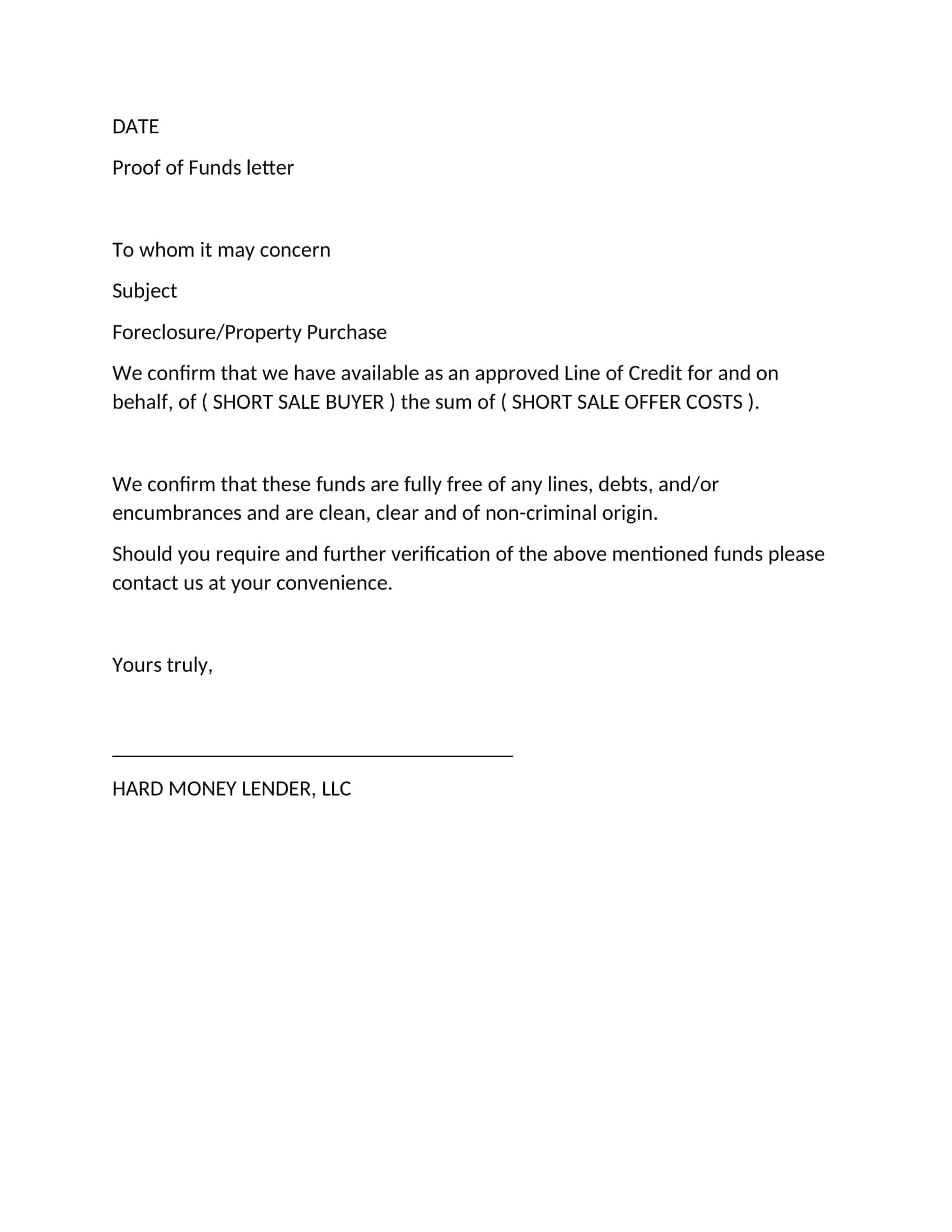

The world of commodity trading, particularly in sectors involving oil, gold, or bulk agricultural products, heavily relies on POF. Buyers often need to present a POF letter to secure a preliminary sales contract (SPA) with a seller or refinery. This is often tied to instruments like Letters of Credit (LC) or Standby Letters of Credit (SBLC), where the POF acts as the underlying foundation confirming the ability to fund the primary instrument if needed.

While bank-issued letters are the gold standard, certain transactions might accept alternative forms, though often with higher scrutiny. For example, documentation from brokerage accounts showing significant margin purchasing power or verifiable statements from regulated trusts can sometimes substitute, but only if the counterparty explicitly agrees to these terms.

Securing an authentic and readily accepted POF letter requires working directly with established financial institutions and understanding their specific protocols. The process is not instantaneous, as banks must verify the source and nature of the funds to comply with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations.

The most straightforward route is usually through your existing primary bank, especially if you maintain a high balance. You will typically need to schedule an appointment with a senior relationship manager. Be prepared to state the exact amount needed and the purpose (e.g., “To be used as earnest money for a real estate purchase”). Banks generally prefer issuing a POF letter when the funds are held in a standard checking or savings account, as these are the most liquid.

For high-net-worth individuals or large corporations, private banks and wealth management firms often offer more personalized service for issuing these documents. These institutions are accustomed to handling sophisticated financial requests and can often tailor the language of the letter to meet specific contractual requirements.

In some intricate global deals, banks may be hesitant to issue a direct POF, especially if the funds are tied up in complex investment vehicles or foreign jurisdictions. In these cases, specialized financial service providers or asset management firms might issue a Bank Comfort Letter (BCL) or a similar guarantee. However, the recipient party must be educated on and explicitly accept these non-bank alternatives, as they carry a different weight than a direct certification from a major commercial bank.

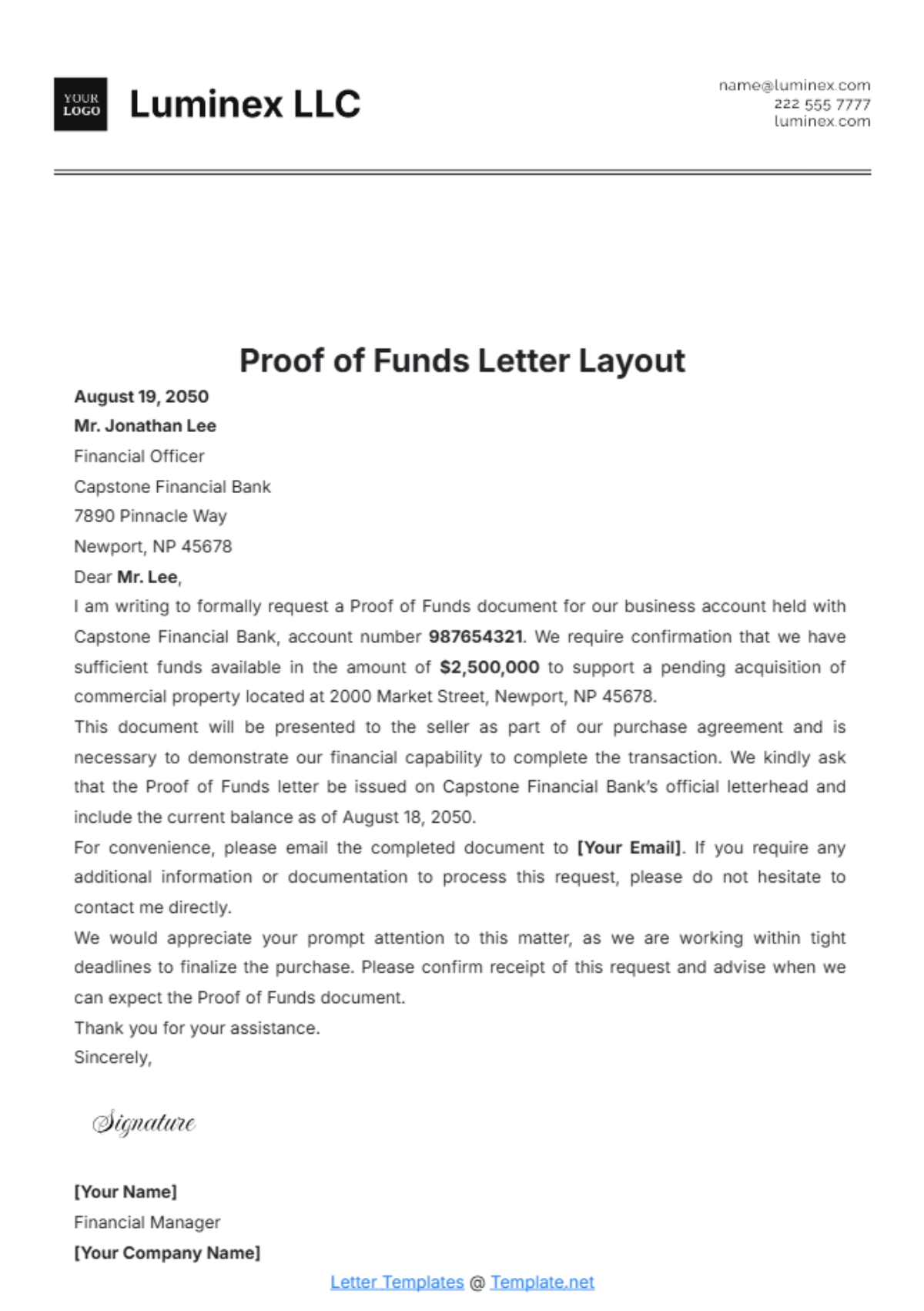

When drafting or requesting a Proof Of Funds Letter Template, precision is vital. Ambiguity breeds doubt. The structure should guide the reader immediately to the critical information: who, what, and how much.

The template must allow for easy modification of several critical variables. If you are using a template provided by your bank, ensure these fields are clear:

One of the most significant pitfalls involves presenting documents that appear fraudulent or outdated. Counterparties are highly experienced in spotting discrepancies. Never attempt to digitally alter a bank-issued letter; the inconsistencies in font, alignment, or watermarks are usually immediately detectable. Furthermore, avoid presenting a POF letter that is older than 30 days unless explicitly permitted by the receiving party, as the liquidity of assets can change rapidly.

The deployment of a Proof of Funds letter carries significant legal weight. It is a representation of present financial standing and must be accurate to avoid serious repercussions.

Trustworthiness (the T in E-E-A-T) is paramount here. Before relying on a POF letter, especially in international transactions, buyers or their representatives should take steps to verify its authenticity. This often involves directly contacting the bank branch listed on the letterhead using a phone number independently sourced from the bank’s official website, not one printed on the letter itself. A simple confirmation call can save a deal from collapsing due to suspicion.

Presenting a false or misleading Proof of Funds letter can lead to severe consequences. If a buyer submits a POF that turns out to be fabricated (often called a “fake POF” or “FPOF”), the seller can potentially sue for damages resulting from the wasted time, legal fees, and lost opportunities caused by the fraudulent submission. In severe cases involving large international trades, this can escalate into criminal fraud investigations. Therefore, the ethical obligation to use only genuine, verifiable documentation cannot be overstated.

Knowing when and how to present your Proof of Funds documentation is a strategic element of negotiation. Presenting it too early might signal desperation or reveal your financial strength prematurely; presenting it too late can cause the deal to stall or result in another buyer being accepted.

In real estate, the POF is typically submitted alongside the initial purchase agreement or Letter of Intent (LOI). It serves as the essential first step in proving qualification before the seller agrees to a detailed inspection or enters into a binding contract. For commodity trading, the POF might be required almost immediately after initial contact to secure a mandate to move forward with deeper discussions regarding terms and shipment schedules. A robust Proof Of Funds Letter Template ensures you are ready when that moment arrives.

When dealing with global commerce, sellers often require funds in their local currency. If your POF is in USD but the transaction is in Euros, you must address this conversion proactively. The most authoritative POF letter will either state the funds in both currencies (with the bank confirming the conversion rate used) or the buyer must quickly provide a secondary document from their financial institution confirming the conversion capacity.

The Proof of Funds letter remains an indispensable tool in modern finance and high-stakes commerce. It functions as the universal language of financial commitment, assuring counterparties that stated intentions are backed by tangible, liquid assets. Mastering the procurement and appropriate presentation of this document—by utilizing a precise Proof Of Funds Letter Template that includes all necessary identifying markers and official certifications—is crucial for any party serious about closing complex deals efficiently. By understanding the necessary components, adhering to ethical verification standards, and timing its presentation strategically, individuals and entities can significantly enhance their credibility and accelerate their path to successful transactions across real estate, mergers, and international trade.