Navigating overwhelming financial obligations can feel isolating, but taking proactive steps, such as utilizing a well-crafted Debt Negotiation Letter Template, is a powerful way to regain control. This essential document serves as the cornerstone of any successful debt settlement strategy, formalizing your offer, outlining your financial constraints, and opening a professional dialogue with creditors or collection agencies. Understanding how to leverage this template effectively transforms a stressful situation into a structured negotiation process, significantly increasing the chances of reducing the total amount owed and establishing manageable repayment terms.

When debt becomes unmanageable, many consumers overlook the strategic advantage of direct communication. However, creditors are often willing to negotiate because receiving any payment is better than pursuing costly and uncertain legal action or writing off the debt entirely. This guide will delve into the crucial components of an effective negotiation letter, provide actionable advice on preparation, and break down exactly how to use a standardized template to achieve favorable settlements. Mastering this communication tool is fundamental to overcoming financial distress.

The effectiveness of any negotiation hinges on preparation and presentation. A poorly constructed communication can be dismissed, while a professional, detailed, and factual letter demands attention. We will explore the specific elements that lend credibility to your request, ensuring that your genuine need for a settlement is understood within the context of the creditor’s business interests.

Sending a formal, written offer is non-negotiable in debt resolution. While phone calls can be useful for initial contact or gathering information, a written communication creates an undeniable paper trail, which is vital for legal and tracking purposes. This formality shifts the interaction from a casual inquiry to a serious business proposal.

Verbal agreements regarding debt settlement are notoriously difficult to enforce or even accurately recall later. A written offer, confirmed by mail or email, establishes a definitive point in time when the negotiation began and what specific terms were proposed. If a creditor verbally agrees to a settlement amount, a written confirmation solidifies that agreement, protecting the consumer from “bait-and-switch” tactics where the agency later claims the initial conversation never happened or was misunderstood.

Using a Debt Negotiation Letter Template immediately signals to the recipient that you are taking concrete steps toward resolution. It shows you have done your homework and are prepared to negotiate seriously. Creditors respect documentation that is clear, cites account numbers correctly, and adheres to a professional format, as it suggests you understand the process, even if you are struggling financially.

Before you even begin filling out your template, robust preparation is necessary. The stronger your foundation of facts, the more persuasive your letter will be. This preparatory phase is where expertise truly shines, transforming a plea into a well-reasoned proposal.

The cornerstone of any successful negotiation is proving your inability to pay the full amount. You must demonstrate a clear picture of your current financial reality. This includes compiling proof of income, essential living expenses (housing, utilities, food, medical needs), and any other outstanding debts.

Creditors assess risk. If they see you have a steady, albeit small, income stream, they might prefer a guaranteed partial payment over nothing. Your letter must clearly articulate why paying the original balance is impossible, supported by these figures.

Before offering to pay anything, you must ensure the debt is valid, accurate, and legally collectible by the entity you are contacting. For collection agencies, this step is crucial. Under the Fair Debt Collection Practices Act (FDCPA), consumers have the right to request debt validation.

If you suspect the debt has passed the statute of limitations for collection in your state, or if the amount seems inflated, your letter should address these issues directly before presenting a settlement offer. Incorrect account numbers or inflated interest charges are powerful leverage points.

How much should you offer? This depends on several factors, including the age of the debt, the creditor’s perceived willingness to settle, and the type of debt (e.g., unsecured debt often settles lower than mortgage debt). Generally, initial offers for collection accounts range from 25% to 50% of the total owed.

It is strategic to start low. A good rule of thumb is to offer an amount you are truly prepared to pay immediately if accepted, but be prepared to increase it incrementally. Never offer an amount you cannot deliver on, as this destroys your credibility instantly.

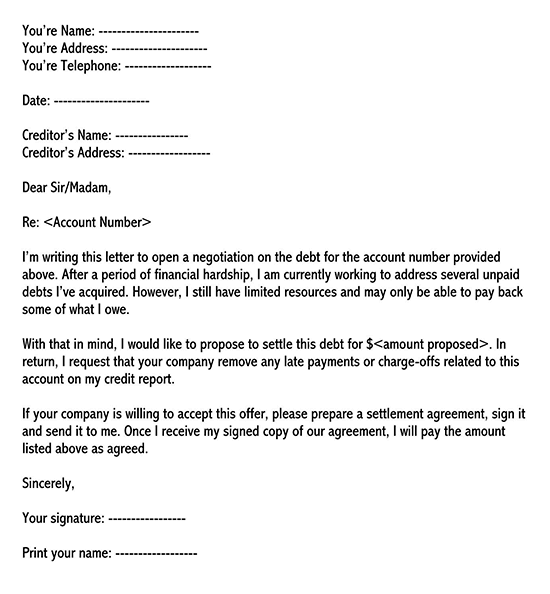

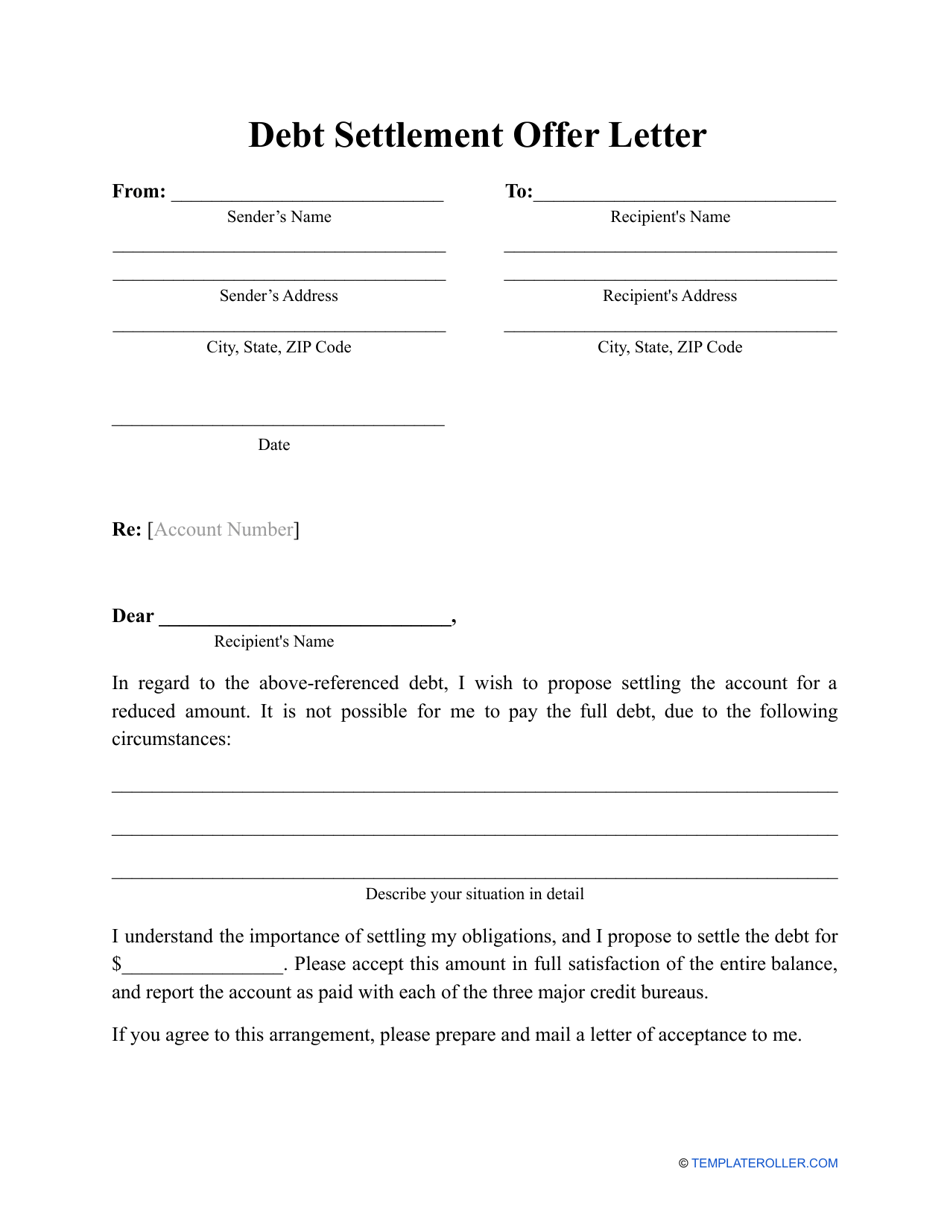

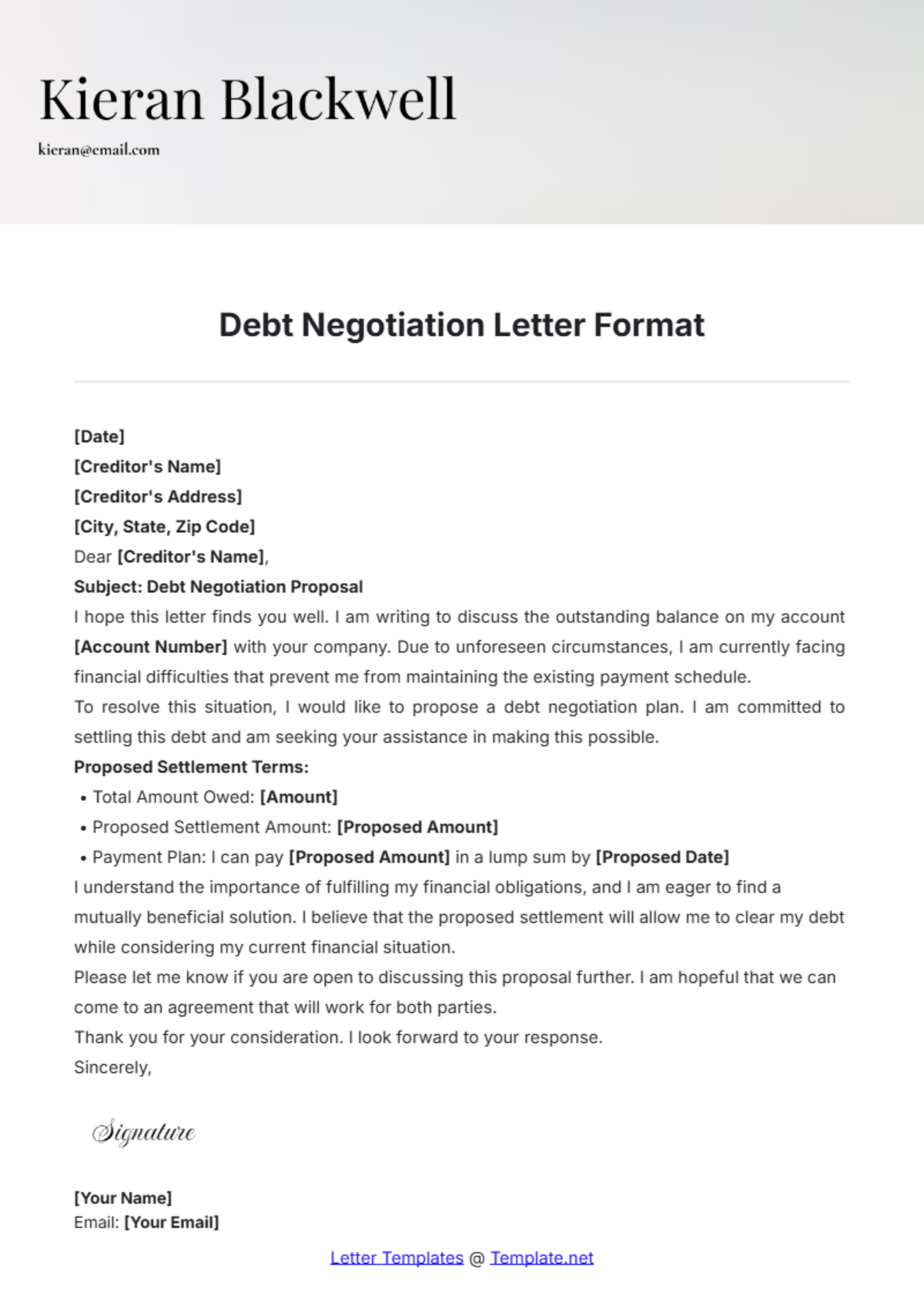

A standardized, professional structure ensures that all necessary information is conveyed clearly and efficiently. A generic Debt Negotiation Letter Template should contain specific, non-negotiable sections to maximize its impact.

This opening section must be pristine. Include your full name, current address, phone number, and email. Critically, clearly list the creditor or collection agency’s name and address, and include the account number in question. State the original creditor (if dealing with a collector) and the current balance claimed.

This immediately confirms you are communicating about the correct debt, saving administrative back-and-forth.

This paragraph clearly states the purpose of the letter: to propose a full settlement for less than the total balance due. Keep it brief and factual. For example: “This letter serves as a formal offer to settle Account Number [XXXXX] in full for the amount of $[Proposed Settlement Amount].”

This is where you present your evidence of financial hardship. Reference the documentation you have compiled (e.g., “As detailed in the enclosed financial summary…”). Explain, without excessive emotional appeal, why paying the full $X is not feasible. Mention job loss, medical expenses, or fixed low income. This provides the context for your lower offer.

Detail the exact settlement amount you are proposing. Crucially, specify the terms of payment. Will this be a lump-sum payment made within 30 days of acceptance? Or are you requesting a payment plan?

If offering a lump sum, you must clearly state that payment is contingent upon receiving written confirmation that the debt will be marked as “Paid in Full” and that the original balance reported to credit bureaus will be updated accordingly. This contingency is vital consumer protection.

Conclude by setting a reasonable deadline for their response, usually 10 to 15 business days. State that if you do not receive a written acceptance by that date, you will consider the offer withdrawn and may explore other financial options. Always state that this communication is an attempt to collect a debt, which is often required under federal regulations like the FDCPA, further solidifying the official nature of your correspondence.

While the core structure remains the same, the leverage points and expectations differ slightly when dealing with collection agencies compared to the original lenders. Expertise dictates tailoring the approach slightly based on the recipient.

Collection agencies typically purchase debt for pennies on the dollar. Their primary goal is quick profit. Because their basis in the debt is often lower, they are generally more flexible on settlement percentages. Your letter should emphasize your request for them to update credit reporting agencies to show “Settled” or “Paid in Full,” as this is a primary concern for consumers dealing with third-party collectors. Always ensure you have validated the debt before settling with a collector.

If you negotiate directly with the bank or credit card company you originally borrowed from, they may have slightly different priorities. They might be more interested in recovering a higher percentage, but they also might be more willing to offer long-term, lower-interest payment plans rather than an outright settlement, especially if the account is relatively new. Your Debt Negotiation Letter Template in this scenario might emphasize a structured repayment plan that fits within your budget rather than a large lump-sum reduction.

Sending the letter is only half the battle; proving it was received and documented is the other critical half. Trustworthiness in this process relies heavily on verifiable proof.

Never send a significant negotiation offer via standard first-class mail only. Always use Certified Mail with Return Receipt Requested. This service costs a few dollars extra but provides you with a green card signed by the recipient, proving the exact date and time they received your formal offer. This documentation is essential if the negotiation stalls or leads to legal escalation.

Maintain a dedicated file—physical or digital—for all debt-related correspondence. Keep a copy of the sent letter (the one you mailed), the return receipt card, and any supporting financial documents. If using email, request a read receipt. This comprehensive record demonstrates your diligence and professionalism.

Respect the deadline you set in the letter. If you haven’t received a written response by the specified date, wait two additional business days, and then initiate a follow-up phone call. Reference the date the letter was sent and received (using your certified mail tracking information) before discussing the proposed settlement terms again.

Even armed with a strong Debt Negotiation Letter Template, consumers frequently make errors that undermine their efforts. Awareness of these pitfalls is key to maintaining control.

The single most common and dangerous mistake is sending money before receiving a written, signed agreement from the creditor accepting your specific settlement terms. If you send a check or wire money before the agreement is finalized, the creditor can cash it, claim it was a partial payment, and still demand the full remainder. Your letter must explicitly state that payment will follow only upon receipt of the written acceptance.

While the situation is inherently stressful, the negotiation letter must remain strictly professional and business-like. Avoid language that expresses anger, despair, or threats (beyond stating you will explore other legal/financial remedies). Stick to objective facts regarding your income, expenses, and proposed resolution.

While bankruptcy might be an eventual option, bringing it up too early in the initial negotiation letter can signal to the creditor that you are not serious about settling outside of bankruptcy court, potentially hardening their stance or reducing their willingness to negotiate substantially. Focus first on proving your current inability to pay outside of that framework.

Once a favorable settlement is reached and documented, the final step is execution. The agreement dictates that the debt is settled for a lower amount, provided you fulfill the payment obligation promptly.

A crucial detail to confirm in your written acceptance from the creditor is how the account will be reported to the major credit bureaus (Experian, Equifax, TransUnion). Ideally, the agreement stipulates the account will be reported as “Paid in Full” or “Settled for Less than Full Balance.” If they agree to a specific reporting term, ensure that is documented. Even if they simply agree to report it as “Settled,” this is significantly better than an “Unpaid Collection” or “Charge-Off” status.

Following up 30 to 60 days after payment to verify the credit report reflects the agreed-upon status is essential for completing the process successfully.

Mastering the art of debt negotiation starts with powerful, professional documentation. By utilizing a structured Debt Negotiation Letter Template, thoroughly preparing your financial evidence, and adhering to strict communication protocols—especially using certified mail—you transform a position of weakness into a structured business proposal. Remember that creditors are businesses seeking recovery, and a well-articulated, evidence-backed offer that benefits both parties is often the fastest path to resolving outstanding financial burdens. Taking this step demonstrates commitment and expertise, moving you significantly closer to financial freedom.