Navigating the complexities of UK tax compliance, particularly within the construction industry, requires meticulous record-keeping. For subcontractors operating under the Construction Industry Scheme (CIS), utilizing an accurate and comprehensive Cis Invoice Template Subcontractor is not merely a best practice—it is a statutory necessity for managing payments and deductions correctly with HMRC. Failure to adhere to the specific requirements for CIS invoicing can lead to delays in payment, incorrect tax withholding, or potential penalties from the tax authority. This specialized invoicing process ensures that the main contractor can accurately account for the 20% or 30% deduction required by the scheme, streamlining administrative burdens for both parties involved in the construction project.

The CIS framework is designed to combat tax evasion within the construction sector by requiring contractors to deduct tax at source from payments made to subcontractors, similar to PAYE but applied to self-employed or limited company subcontractors. Understanding the nuances of what must appear on these documents separates compliant businesses from those facing audit scrutiny. A well-structured template acts as the primary evidence supporting the declared income and deductions when submitting CIS returns.

This detailed guide will explore every essential element required in a Cis Invoice Template Subcontractor, discuss the critical difference between gross and net payment status, and provide actionable advice on streamlining your billing process to maintain full compliance with HMRC regulations, ensuring a smooth cash flow cycle.

Before diving into the specifics of the template itself, it is crucial to solidify the foundational knowledge surrounding CIS. The scheme applies to all construction operations carried out in the UK, from demolition and site preparation to the erection and finishing of buildings. As an expert in financial compliance for this sector, it’s vital to recognize that the responsibility for deduction lies squarely with the contractor—the entity paying for the work. The subcontractor, therefore, must provide the documentation necessary for the contractor to fulfil this duty correctly.

The most significant factor influencing how a subcontractor should invoice is their payment status as registered with HMRC. There are generally two main deduction rates:

Your invoice must clearly reflect which scenario applies, although the invoice primarily serves to inform the contractor so they can apply the correct deduction based on their internal verification.

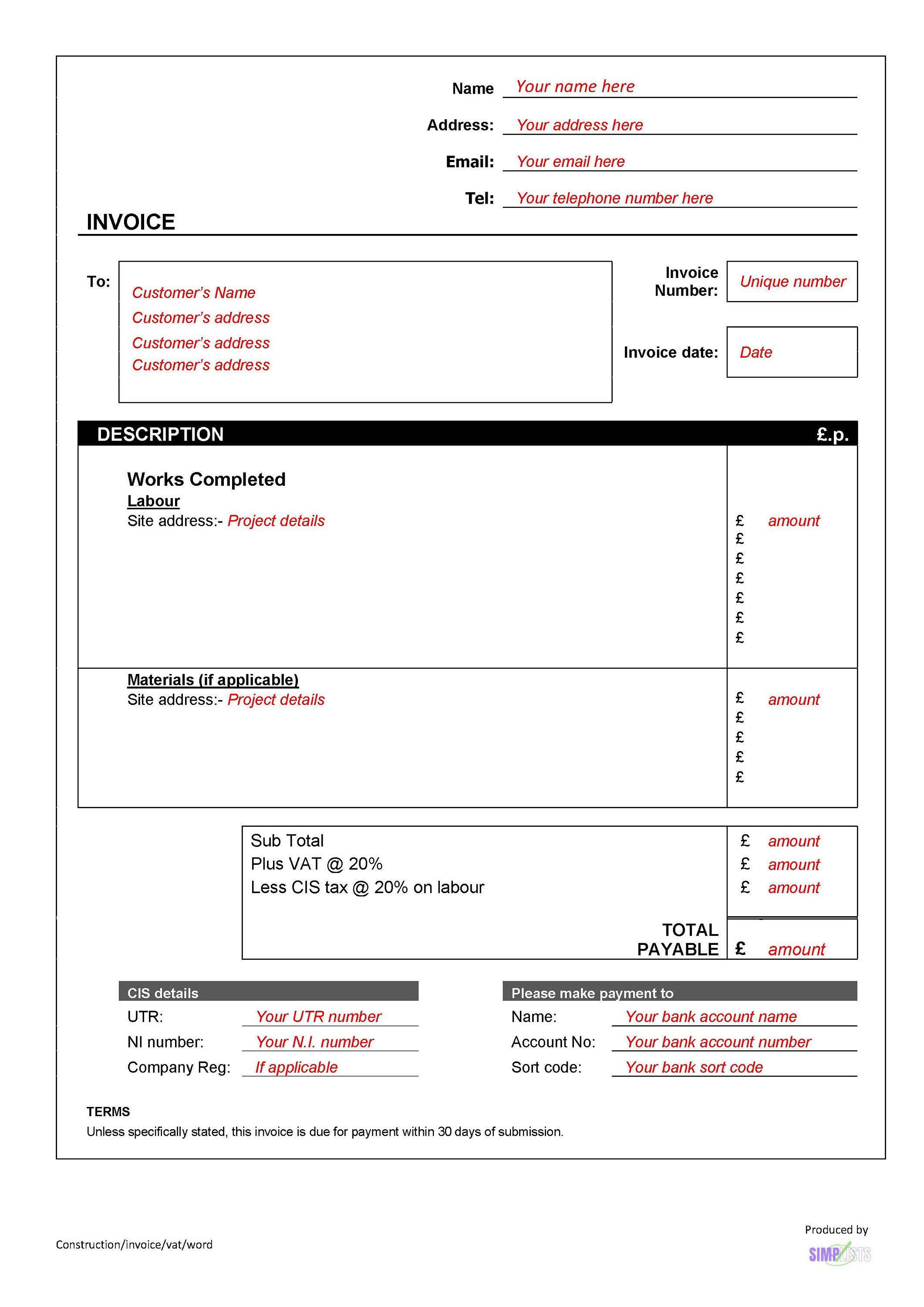

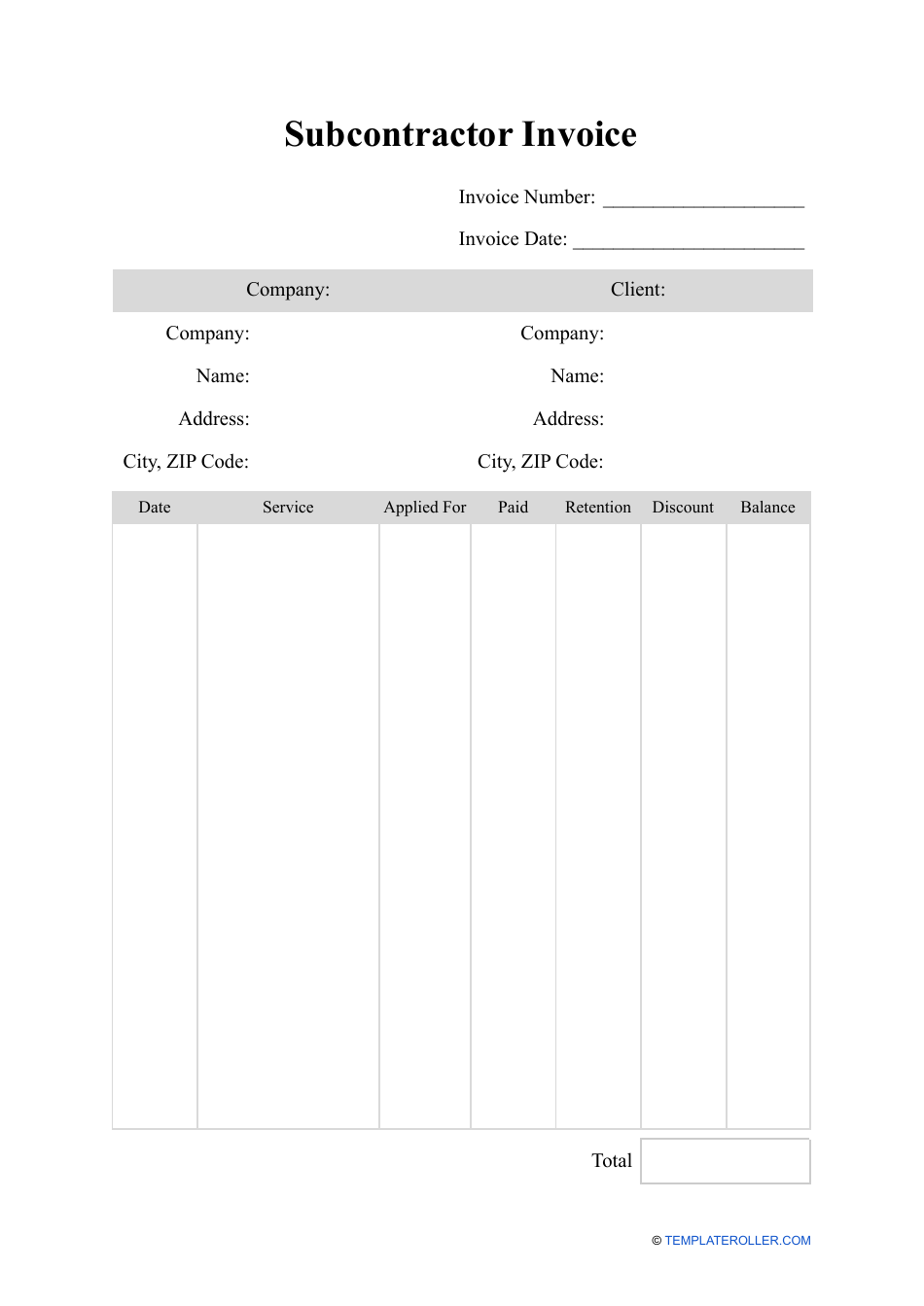

A standard commercial invoice is insufficient for CIS compliance. Every Cis Invoice Template Subcontractor must contain specific data fields required by HMRC for verification and reporting purposes. Omitting even a seemingly minor detail can cause the contractor to apply the wrong deduction rate or reject the invoice entirely, resulting in payment delays.

Accuracy in identifying both parties is non-negotiable. This section must clearly establish the legal entities involved in the transaction.

This is perhaps the most critical piece of information distinguishing a CIS invoice from a standard one. When the subcontractor registers for CIS (or when the contractor verifies them), HMRC provides a unique verification number.

Standard professional practice applies here, but it’s crucial for audit trails:

The invoice must clearly break down the services provided. Ambiguity here often leads to disputes or payment hold-ups.

This is the core compliance section of the Cis Invoice Template Subcontractor. It must explicitly show how the gross amount transitions to the net payment due.

A professional layout ensures readability and minimizes the chance of human error during processing. When designing your template, think in terms of blocks of information corresponding to HMRC’s required flow of data.

The top section should house all identifying information. Use clear, distinct sections for the ‘Issuer’ (subcontractor) and the ‘Recipient’ (contractor). Ensure your UTR is prominently displayed near your contact details, as this is often the first piece of data the contractor’s accounts department seeks for verification checks.

This central area requires meticulous attention to detail. If you are working on a large project spanning multiple months, it is essential to link the invoice clearly to the specific Contract Number or Works Order Reference provided by the main contractor. This cross-referencing capability is vital for linking the invoice to the contractor’s CIS ledger.

The bottom of the invoice serves as a final instruction and declaration area. While not strictly mandatory for the CIS deduction calculation, including clear payment terms (e.g., “Payment due within 30 days of invoice date”) is essential for cash flow management. Furthermore, it is highly beneficial to include a statement affirming compliance, such as: “This invoice complies with the requirements of HMRC’s Construction Industry Scheme (CIS).”

The UTR (Unique Taxpayer Reference) is the backbone of UK self-assessment and CIS compliance. For a subcontractor, ensuring their UTR is correct on every invoice is paramount. If a contractor attempts to verify a subcontractor’s status using an incorrect UTR, the verification will likely fail, forcing the contractor to apply the default 30% deduction rate.

The process begins when the subcontractor contacts HMRC (or their contractor does) to verify their status before submitting the invoice. HMRC confirms whether the subcontractor is registered and what rate applies (0%, 20%, or 30%).

If the subcontractor has Gross Payment Status (0% deduction), they must ensure their invoice reflects this by showing zero tax deducted, and the contractor must honor this, provided the verification process confirms the status. If the subcontractor is simply registered (20% deduction), this must be clearly shown.

Expert Insight: Many experienced subcontractors integrate a small note on their template stating: “Verified with HMRC on [Date] under Verification Number: [Number].” While the contractor should verify independently, pre-filling this information streamlines their internal audit process, often leading to faster approvals.

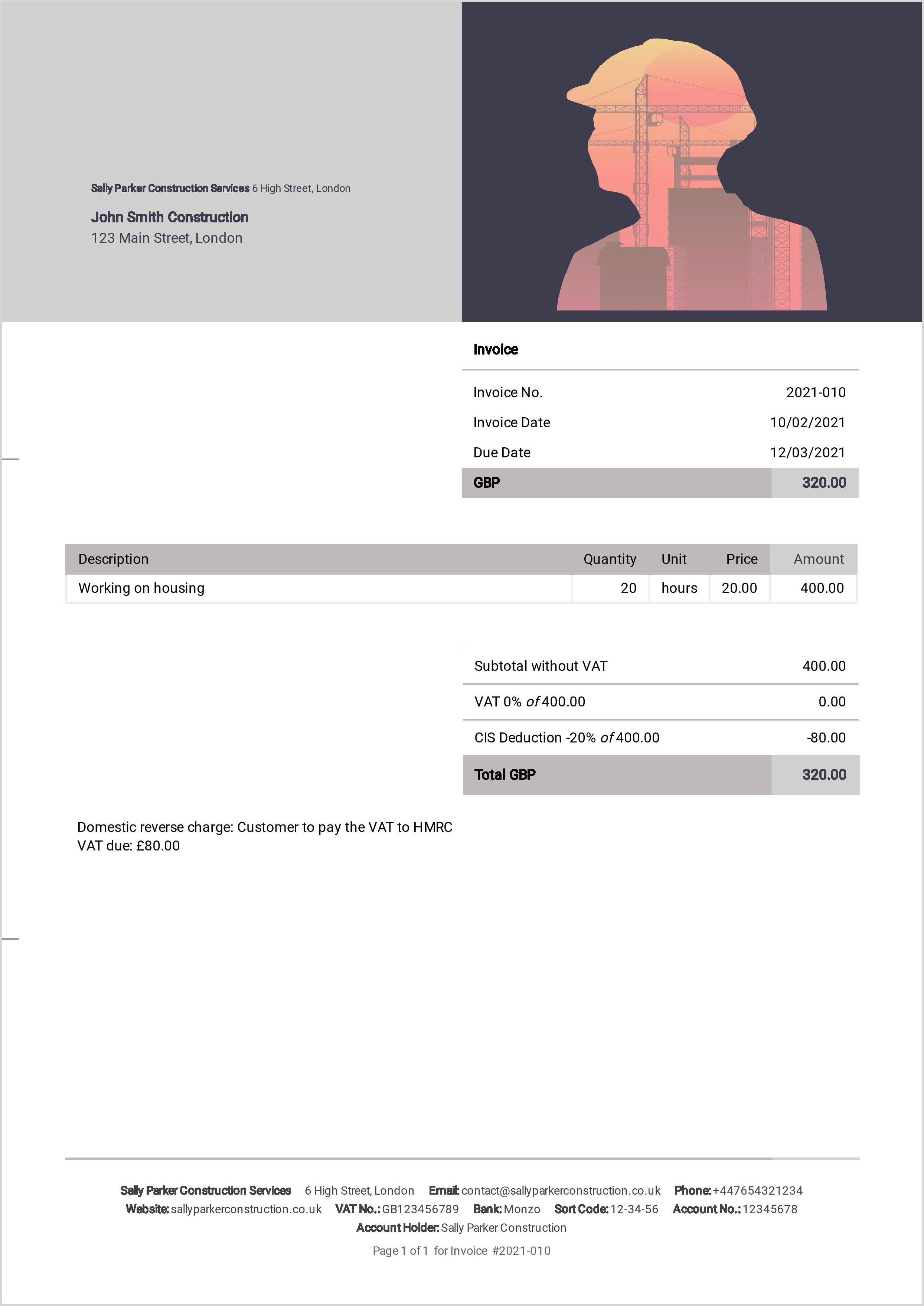

A frequent point of confusion for subcontractors is how Value Added Tax (VAT) interacts with the CIS deduction. As an expert writer on this topic, it’s crucial to clarify that CIS deductions are calculated only on the value of the construction service itself, excluding VAT.

If you are VAT registered, your invoice must show three separate amounts:

For example, if you invoice £1,000 for labour (subject to CIS) plus £200 VAT (20% rate), the CIS deduction is taken from the £1,000. If you are on the 20% deduction scheme, £200 is deducted for CIS tax, leaving a net payment of £800 for the labour, plus the £200 VAT payment separate—though VAT payments are generally handled through your standard VAT return process, not usually paid directly to the subcontractor via the CIS mechanism. The contractor pays you the gross amount minus the CIS tax.

While paper templates or basic spreadsheets suffice for very small operations, scaling businesses benefit immensely from specialized accounting software designed to handle CIS requirements automatically.

Modern accounting platforms (like Xero, QuickBooks with CIS add-ons, or dedicated construction accounting packages) automate several painful manual steps:

For subcontractors, utilizing a digital Cis Invoice Template Subcontractor ensures that every invoice issued adheres to the latest HMRC specifications without requiring constant manual cross-referencing of tax law updates.

Even with a solid template, errors creep in. Being aware of the most frequent mistakes allows subcontractors to proactively safeguard their revenue stream.

The contractor’s biggest risk is under-reporting the tax they deducted. If they calculate the deduction incorrectly (e.g., deducting 20% when they should have used 30% because verification failed), they face penalties. Submitting a clear invoice highlighting the intended rate (based on verification) minimizes this risk. If the invoice shows a 0% deduction, the contractor must have valid verification documentation or risk liability.

The invoice itself triggers the payment process. Delays in submitting a compliant invoice mean delays in payment. If you wait until the end of the month to generate invoices for all jobs, you are unnecessarily delaying your cash flow, especially if the contractor has a 30-day payment term starting from the invoice date. Aim to invoice work immediately upon completion of milestones or at the agreed invoicing cycle point.

Mastering the creation and submission of accurate invoicing documentation is fundamental to the financial health of any subcontractor operating under the UK’s Construction Industry Scheme. The Cis Invoice Template Subcontractor is more than just a billing document; it is a critical compliance tool that facilitates HMRC oversight and ensures prompt payment by the main contractor. Key requirements remain consistent: clear identification of both parties, inclusion of the subcontractor’s UTR, the crucial CIS verification number, and an explicit breakdown of the gross amount versus the CIS tax deduction applied. By adopting standardized, detailed templates—preferably through digital solutions that automate verification checks and rate application—subcontractors can move confidently through projects, secure in the knowledge that their documentation supports full tax compliance and optimized cash flow management.