Understanding the intricacies of lending and borrowing money, whether between individuals or businesses, often necessitates a formal, legally binding agreement. For those seeking clarity and security in such transactions, utilizing a well-drafted Promissory Note Template is the essential first step. This document serves as a powerful tool, meticulously outlining the terms under which a borrower promises to repay a specified sum of money to a lender on a specific date or on demand. Its importance cannot be overstated in establishing a clear paper trail, minimizing potential disputes, and ensuring enforceability should repayment falter.

A promissory note moves an informal handshake agreement into the realm of formal contractual obligation. It provides both parties with peace of mind: the lender knows the exact repayment schedule, interest rate, and consequences of default, while the borrower clearly understands their financial obligations moving forward. As financial literacy and legal compliance become increasingly crucial, grasping the components of this foundational document ensures that any money transaction, large or small, is handled with professional rigor and legal soundness.

This comprehensive guide will delve deep into what constitutes a robust promissory note, detail the critical elements that must be present, explore when and why you might need one, and offer insights into leveraging a reliable template effectively. Our goal is to empower you with the knowledge necessary to create, execute, and manage these vital financial instruments confidently.

A promissory note, often referred to simply as a “note,” is essentially a written IOU that contains a formal promise by one party (the maker or issuer) to pay a specific sum of money to another party (the payee or lender). It is a negotiable instrument, meaning it can often be transferred to another party, although for standard private loans, it typically remains between the original signatories.

While often confused, a promissory note and a formal loan agreement serve distinct primary functions. A standard loan agreement is typically more expansive, detailing collateral, covenants, default remedies, and specific warranties. In contrast, the promissory note focuses squarely on the promise to pay—the principal amount, the interest rate, and the repayment schedule. In many commercial settings, a promissory note might be attached to or governed by a broader loan agreement, but the note itself carries the direct promise of repayment. This focused nature makes the promissory note a clean, powerful document for straightforward debt obligations.

A critical distinction in any lending scenario is whether the debt is secured or unsecured. A secured promissory note means the borrower has pledged an asset (like real estate or a vehicle) as collateral. If the borrower defaults, the lender has the legal right to seize and sell that collateral to recover their losses. Conversely, an unsecured promissory note relies solely on the borrower’s promise to pay and their general creditworthiness, offering the lender no specific asset to claim in case of default. The structure of the template used must clearly reflect this distinction.

To ensure maximum enforceability and clarity, any template you select or customize must contain several non-negotiable elements. These components form the legal backbone of the agreement, leaving little room for ambiguity if a dispute arises.

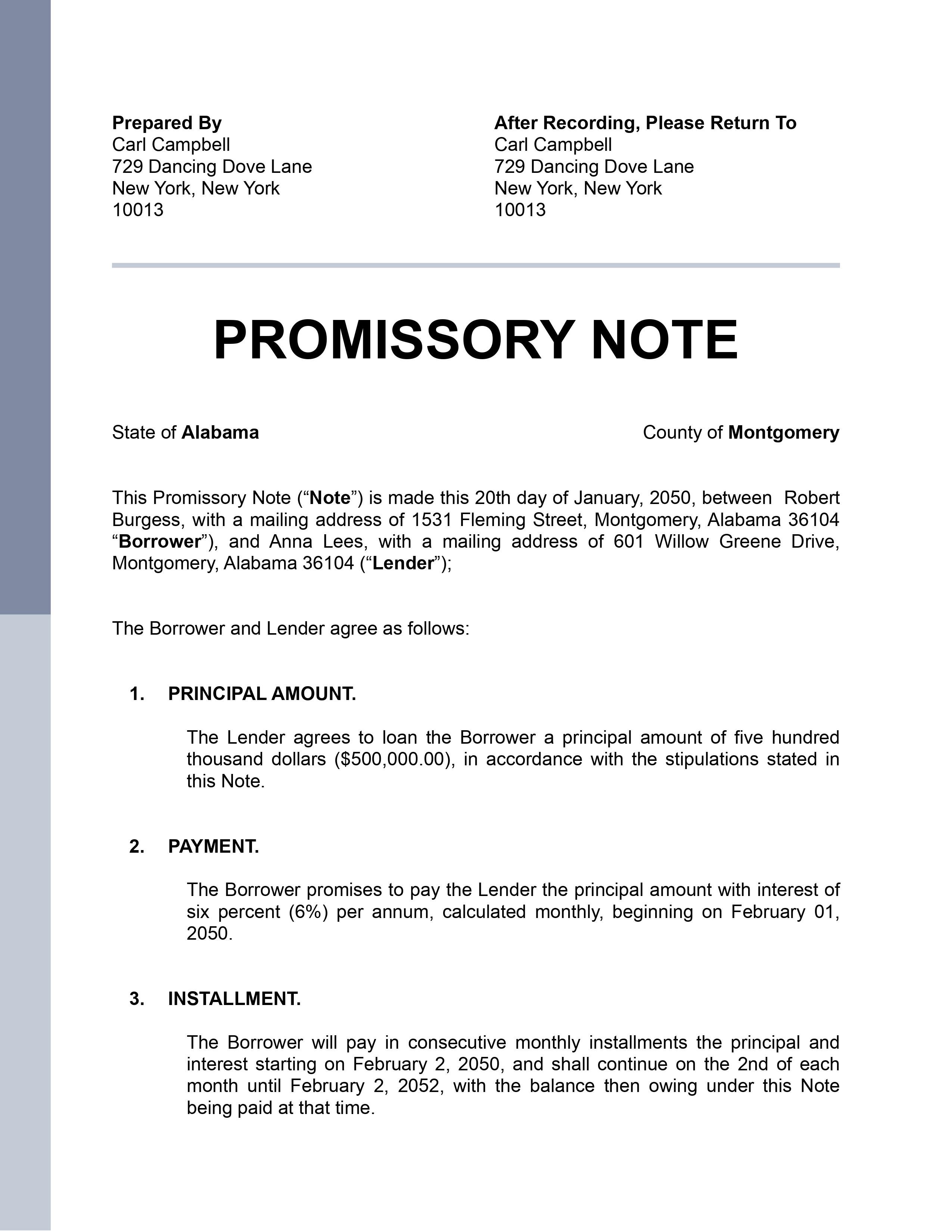

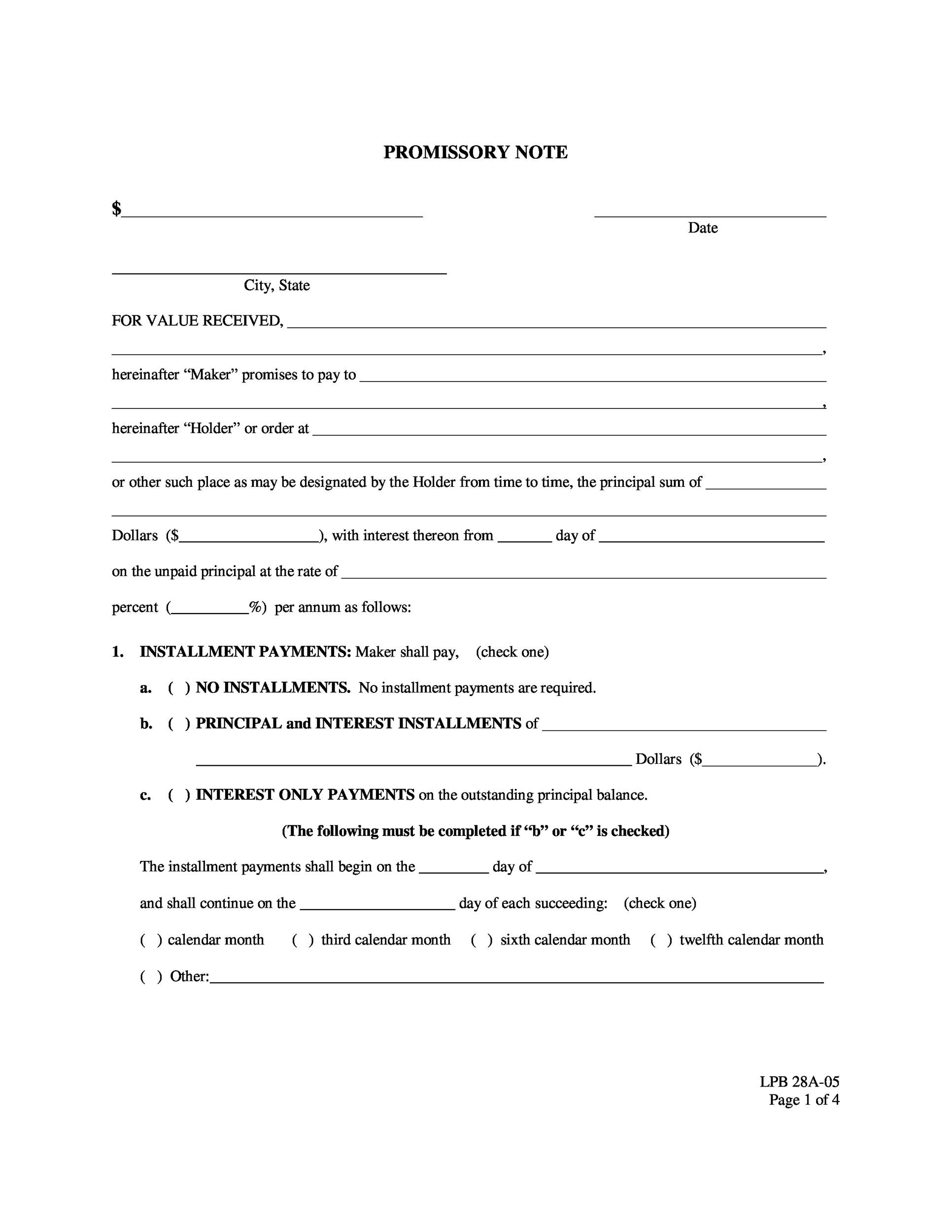

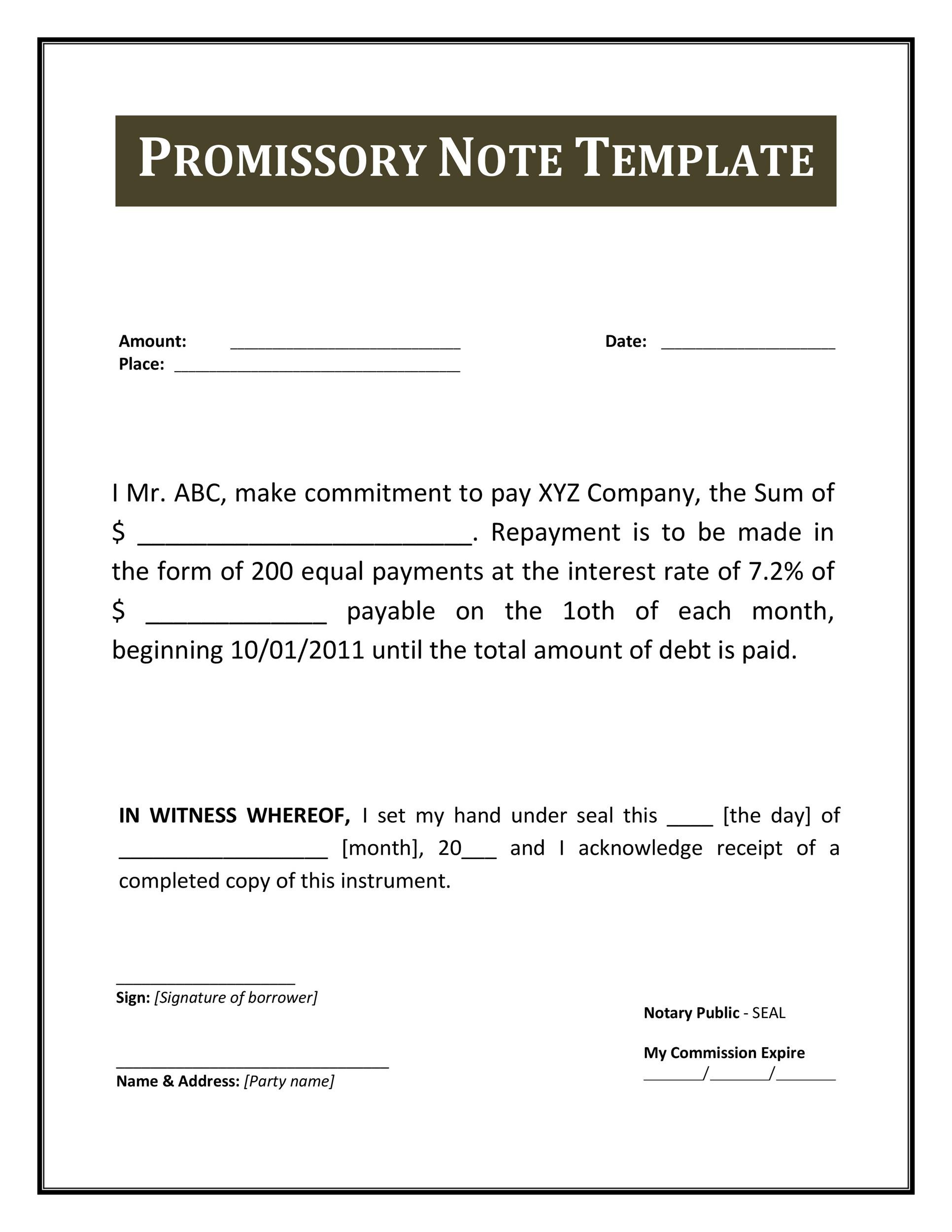

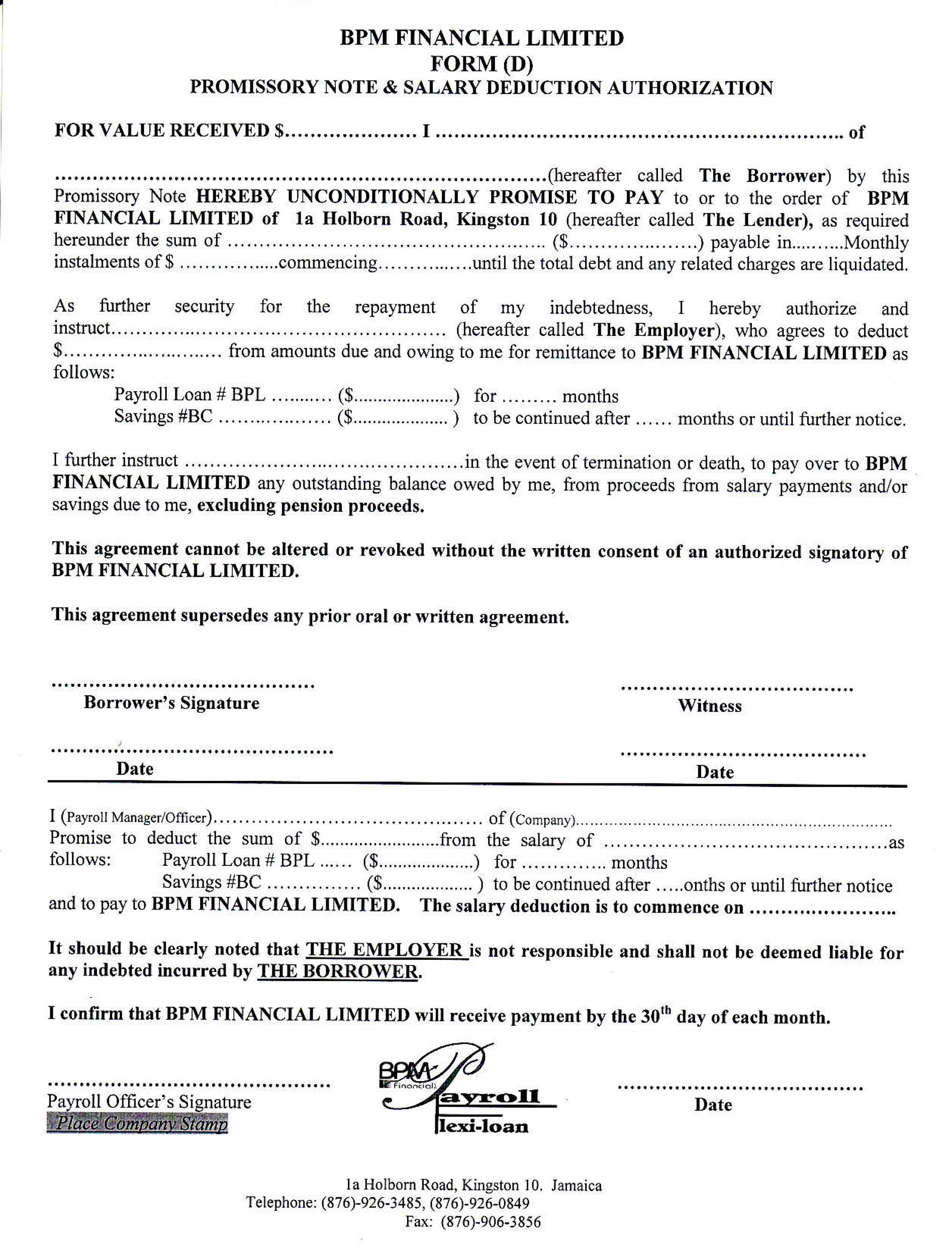

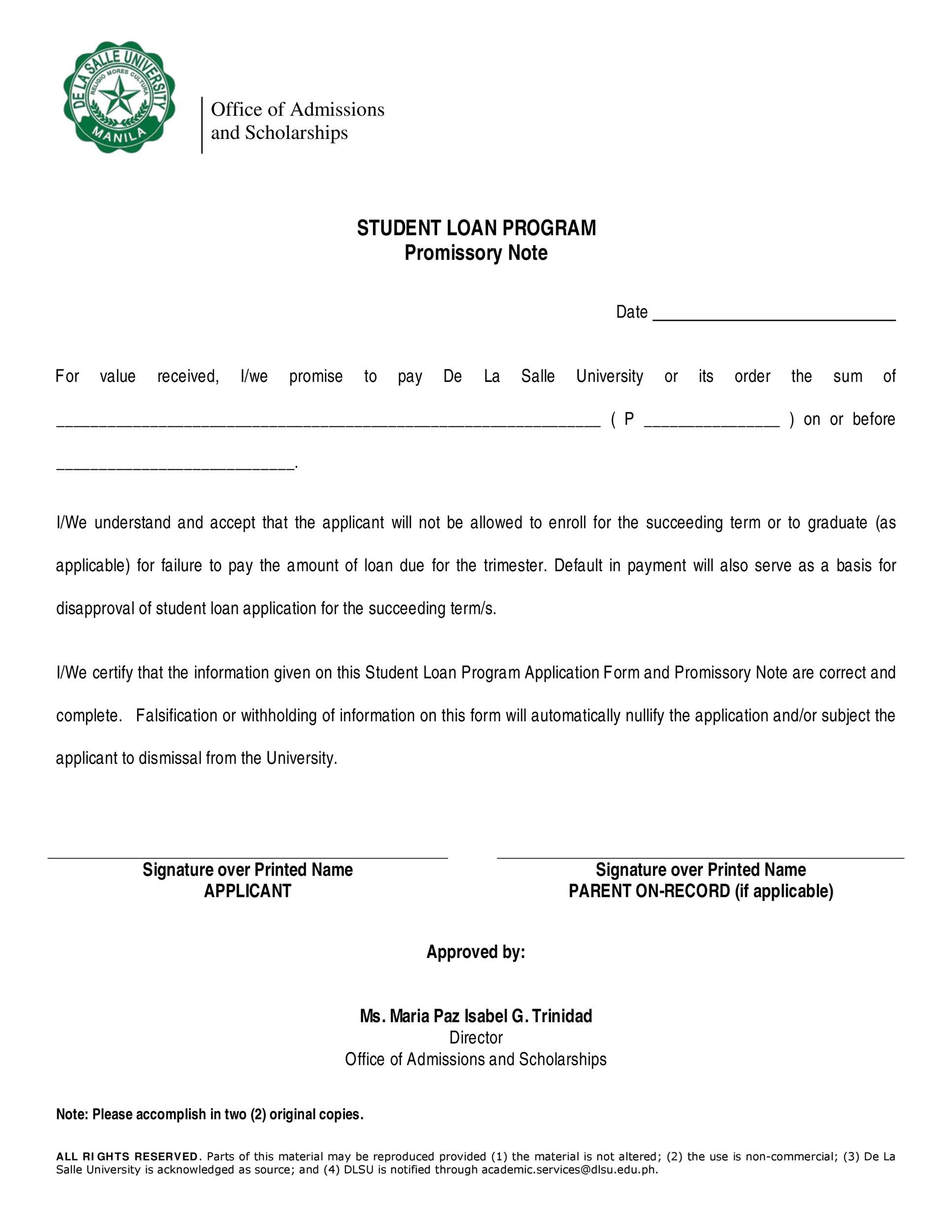

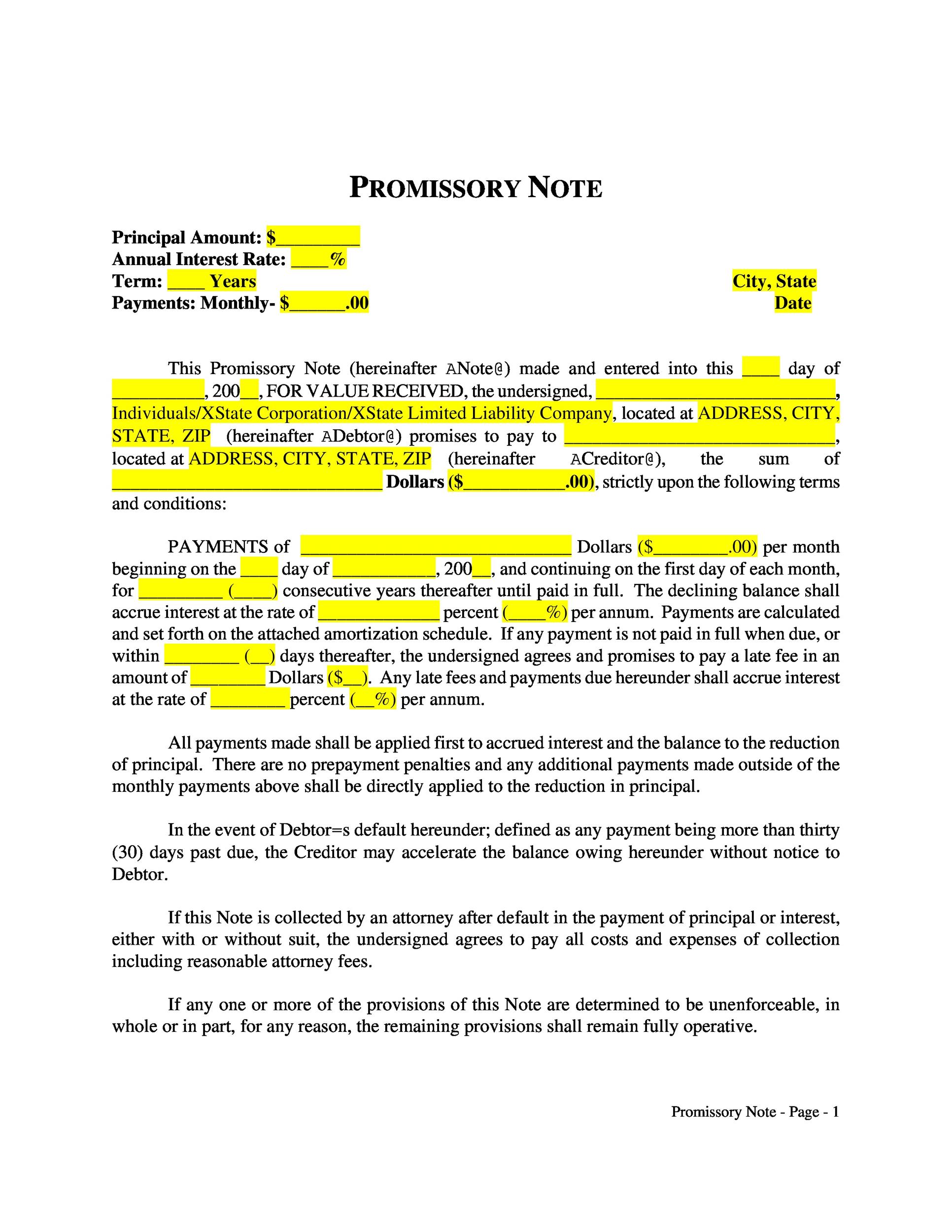

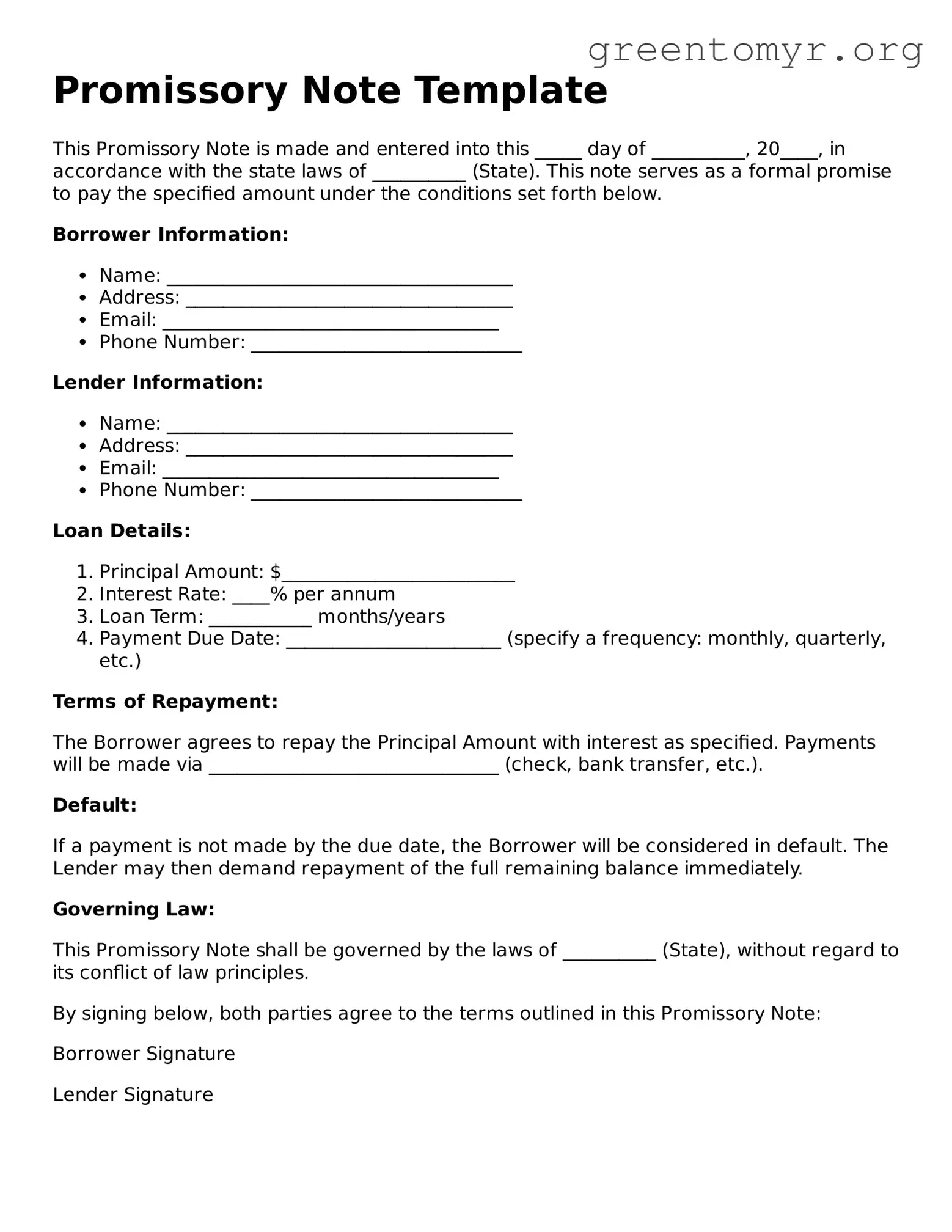

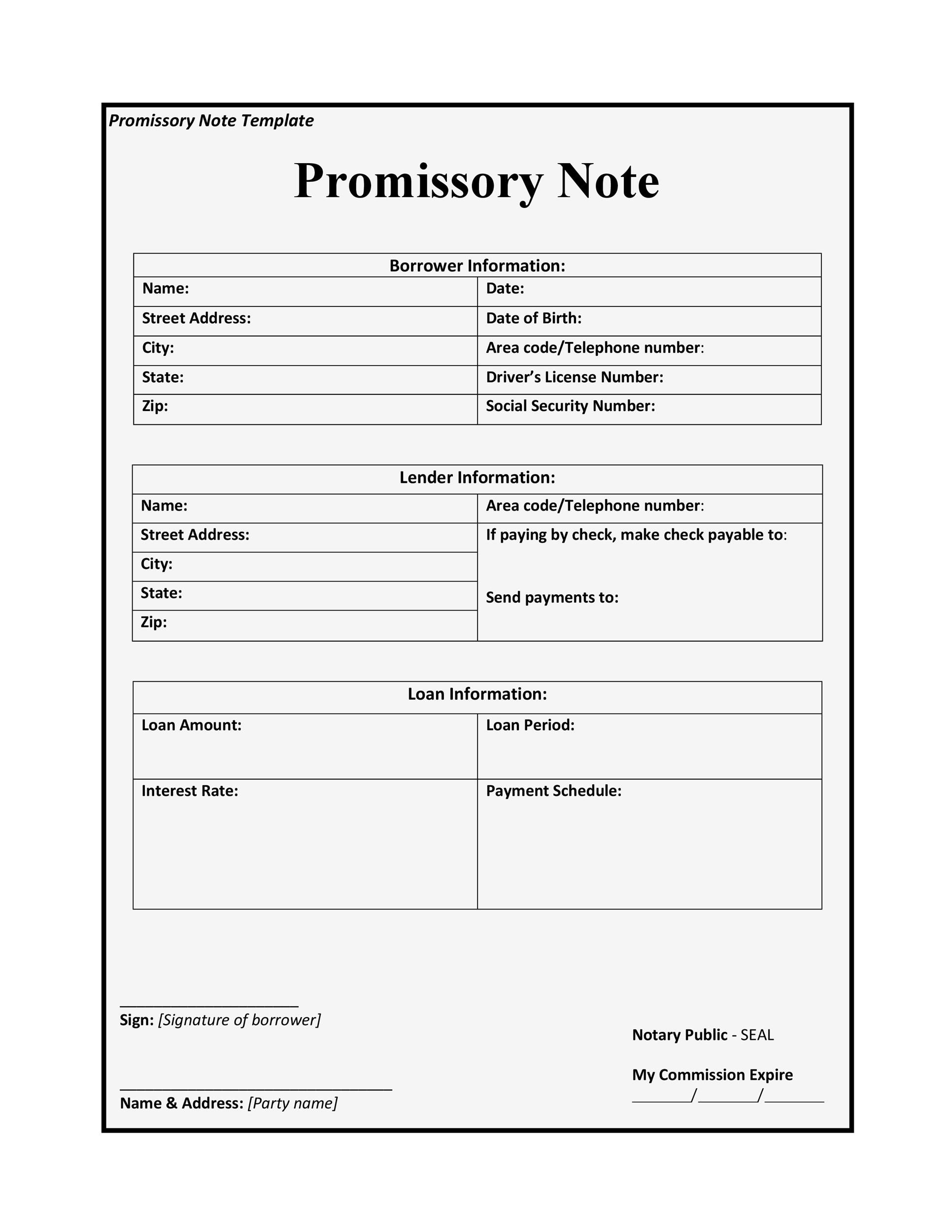

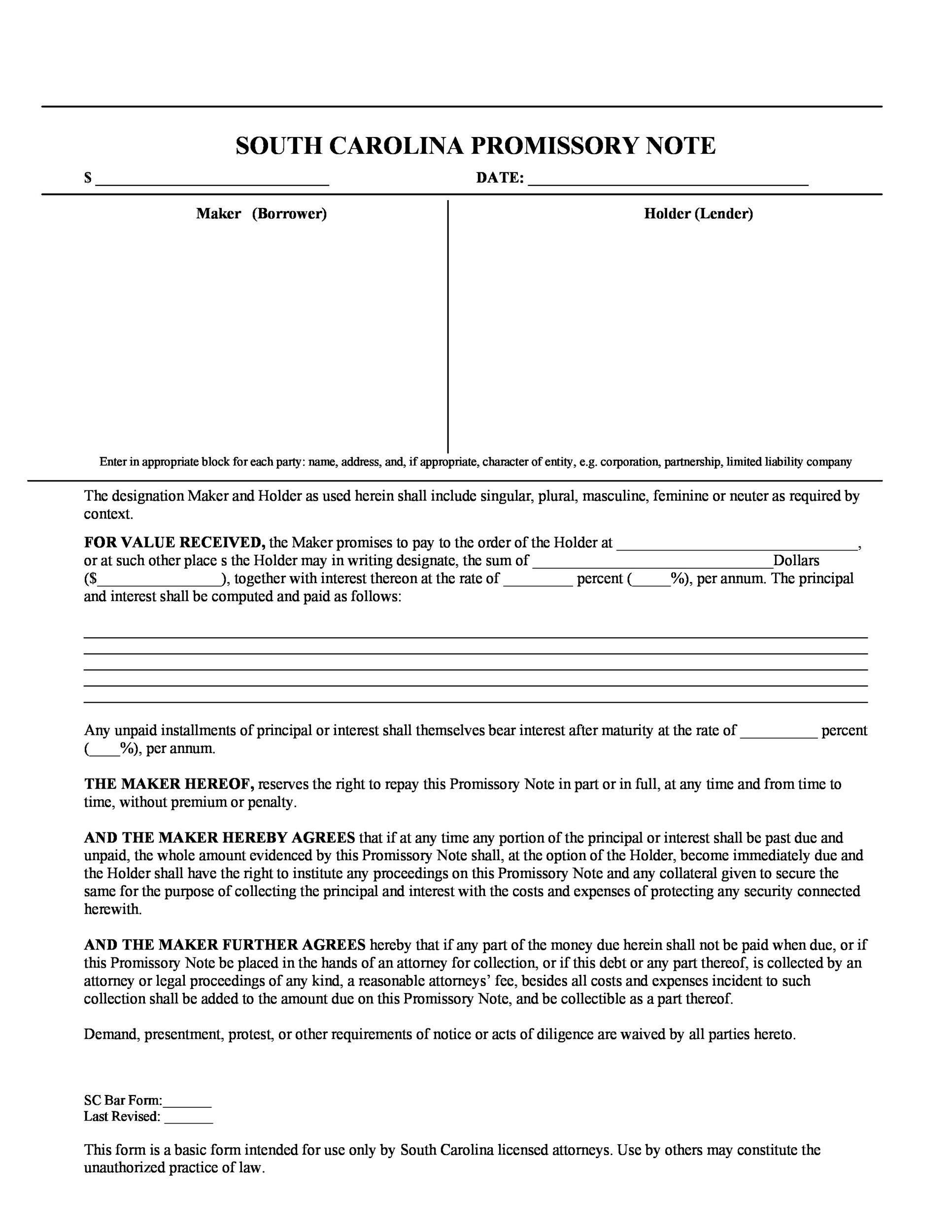

The note must clearly identify who owes the money and who is owed the money. This requires the full legal names and current addresses of both the Maker (the borrower) and the Payee (the lender). If either party is a corporation or business entity, their full registered legal name must be used.

This section details the core financial obligation. The principal amount (the original sum borrowed) must be stated precisely, often both numerically and written out in words, to prevent alterations. Equally important is the interest rate. If interest is charged, the rate must be specified—usually an annual percentage rate (APR). Furthermore, the note should clarify whether the interest is simple or compounded, and when it begins to accrue.

Clarity on when and how the money will be paid back is vital. This section must define:

A robust template addresses what happens when payments are missed. This includes specifying any late fees—and ensuring these fees comply with state usury laws. More importantly, the note must define what constitutes an event of default (e.g., missing three consecutive payments, filing for bankruptcy) and outline the remedies available to the lender, such as demanding immediate payment of the entire outstanding balance (acceleration clause).

Borrowers often wish to pay off the loan early to avoid future interest charges. The note template must explicitly state whether prepayment is allowed and, if so, whether there are any penalties associated with paying the loan off ahead of schedule. If no mention is made, many jurisdictions assume prepayment is allowed without penalty, but explicit confirmation is best practice.

The flexibility of the promissory note format allows it to be adapted for a wide array of financial transactions. Choosing the right structure within your Promissory Note Template is key to matching the document to the specific needs of the loan.

When lending money to family or close friends, people often rely on trust. However, even the closest relationships can be strained by unmet financial expectations. Using a template ensures that the informal understanding is formalized. For these personal loans, an unsecured note is common, often featuring a lower or even zero interest rate, though the principal and repayment schedule must still be rigid.

Small businesses often use promissory notes when borrowing from angel investors, securing short-term working capital, or extending credit to customers who need to pay for goods or services over time. In these commercial contexts, secured notes are more frequent, often tied to business assets. The terms here must be highly detailed regarding commercial covenants.

While mortgages or deeds of trust handle primary real estate financing, promissory notes are crucial for secondary or junior financing, such as seller financing or home equity lines of credit (HELOCs) structured as a note. In these cases, the note is inextricably linked to a mortgage document that secures the debt against the property.

For a promissory note to be fully effective, it must adhere to the laws of the governing jurisdiction. This is where expertise in drafting—or selecting the right template—becomes paramount for E-E-A-T.

Every valid note must specify which state’s laws will govern its interpretation and enforcement. This is the Governing Law clause. If the lender is in California and the borrower is in Texas, the note must clearly state which state’s contract law applies. This clause significantly impacts the enforceability of elements like interest rate caps and collection procedures.

One of the most critical legal checks involves usury laws. These laws, which vary significantly by state, dictate the maximum allowable interest rate that can be charged on a loan. If a promissory note charges an interest rate exceeding the legal maximum for that type of loan in that jurisdiction, the entire note—or at least the interest component—may be deemed void and unenforceable by a court. An expert template will often prompt the user to verify applicable state limits.

While many simple promissory notes do not legally require notarization to be valid between the two signing parties, having the signatures notarized significantly boosts the trustworthiness and authority of the document should it ever need to be presented in court. Notarization confirms the identity of the signatories at the time of signing, making it much harder for a borrower to later claim they did not sign the document.

Selecting a reliable Promissory Note Template is just the starting point; proper execution is what grants the document its power. Follow these steps to ensure you create a legally sound instrument.

Determine if you need a simple interest-bearing note, a zero-interest note, a demand note, or a secured note. Your choice dictates the specific clauses you will need to include or exclude.

Systematically fill in every blank field provided by the template. Double-check names, addresses, exact dollar amounts, and the specific date the agreement is signed. Accuracy here prevents future litigation over simple clerical errors.

Review the default section thoroughly. If you are the lender, ensure the penalties and the acceleration clause (the right to demand immediate full repayment upon default) are realistic yet firm enough to motivate timely payment. If you are the borrower, ensure the default conditions are achievable and that you understand the remedies outlined.

Before finalizing, verify that the template’s clauses regarding interest rates and late fees align with the governing state’s usury laws. If the template is generic, you may need an attorney specializing in local law to review the interest and penalty clauses. This step bolsters the document’s legal authority.

Both parties must sign and date the document. Ideally, have signatures witnessed or notarized. Crucially, make physical and digital copies for both the lender and the borrower. Keep the original, signed version in a secure location. Every subsequent payment made should also be documented with a separate payment receipt or a notation signed by the lender directly on the original note, showing the remaining principal balance.

While drafting a simple IOU might seem easy, the complexity arises in ensuring all contingencies—like what happens if the borrower dies, or if payments are made sporadically—are covered. This is where the expertise embedded in professional templates proves invaluable.

An expert-designed Promissory Note Template anticipates common pitfalls. It includes boilerplate language regarding jurisdiction, assignment of the note, waivers of presentment, and modifications, which an amateur drafter might overlook. These clauses are essential protective measures that bolster the lender’s position. For example, a standard template will often include language stating that any amendments must be in writing and signed by both parties, preventing later disputes based on verbal agreements.

For business or significant personal loans, using a professionally structured document immediately lends authority to the transaction. It signals to all parties that the debt is being taken seriously and managed formally. This formality often encourages better borrower behavior because the obligation is clearly defined in a legally recognized format.

The promissory note remains an indispensable tool in modern finance, bridging the gap between informal lending and formal debt contracts. By understanding the critical components—from precise identification of parties and principal amounts to the legal implications of governing law and usury compliance—you transform a simple promise into a powerful, enforceable legal instrument. Utilizing a well-structured Promissory Note Template ensures that all necessary safeguards are in place, fostering trust while protecting the financial interests of both the lender and the borrower. Treat the creation and execution of this document with the seriousness it deserves, and you will establish a clear, authoritative record for any money transfer.